On March 28, 2026, the Hanoi People’s Council approved a resolution on the city’s 2026-2030 Five-Year Financial Plan, establishing the framework for local budget revenues, expenditures, and borrowings over the next five years. Under the Plan, total local budget revenue is projected to exceed VND1,403 trillion ($54 billion), while total expenditure is expected to surpass VND1,533 trillion ($59 billion), resulting in a budget deficit of VND130.3 trillion ($5 billion).

Measuring fiscal capacity

To finance the deficit and meet principal repayment obligations, Hanoi’s total borrowing requirement has been set at approximately VND134.5 trillion ($5.2 billion).

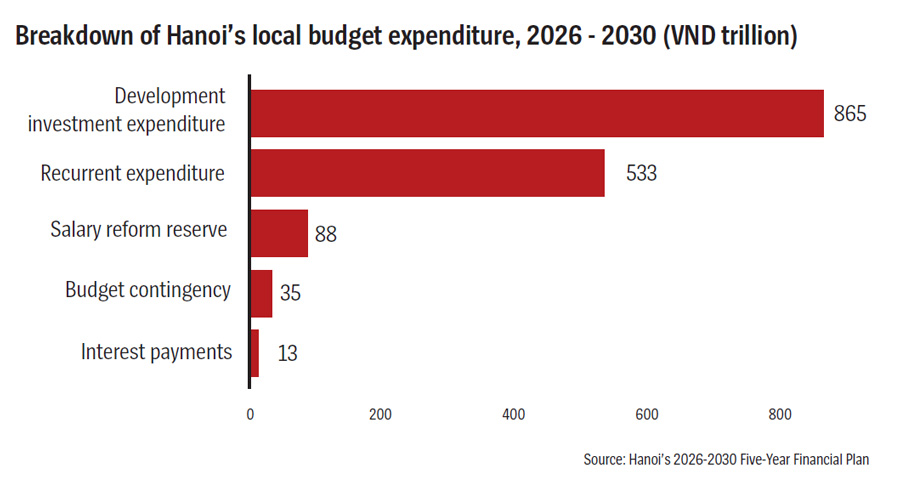

Of the more than VND1,533 trillion ($59 billion) in planned expenditures, Hanoi expects to allocate VND864.7 trillion ($33.3 billion), or 56.4 per cent, to development investment, while VND533.3 trillion ($20.5 billion), or 34.8 per cent, will be earmarked for recurrent spending. The remainder will go to interest payments, public-sector wage reform, budget contingencies, and the financial reserve fund. Compared with the 2021-2025 period, Hanoi’s planned development investment has increased by approximately 33 per cent, from VND650.7 trillion ($25 billion). Over the next five years, the city plans to implement 2,755 projects, including 1,878 city-level projects and 877 commune-level projects.

Notably, the financial plan indicates that Hanoi still has considerable fiscal headroom. Under the resolution, the maximum outstanding local government debt during the period is capped at VND325.6 trillion ($12.5 billion), while outstanding debt at the end of the period is projected to stand at only VND141.6 trillion ($5.4 billion); equivalent to 43.5 per cent of the permitted ceiling.

This means that even after executing its planned borrowing for 2026-2030, Hanoi will still have approximately VND184 trillion ($7.1 billion) in additional borrowing capacity within its statutory debt limit. This provides an important fiscal buffer, allowing it to mobilize additional funding for development projects when necessary, provided it complies with the Law on the State Budget and maintains its debt repayment capacity.

However, less than three months after the financial plan was approved, Hanoi simultaneously broke ground on five new urban railway lines, on June 22. Together, the projects span approximately 303.5 km, carry a preliminary investment estimate of more than VND1,300 trillion ($50 billion), and are to be largely completed by 2030.

Compared with the fiscal targets approved by the Hanoi People’s Council, the preliminary investment cost of the five metro lines is equivalent to approximately 93 per cent of the city’s total projected budget revenue and around 85 per cent of its total budget expenditure for the entire 2026-2030 period. More strikingly, the investment is roughly 1.5-times larger than the entire VND864.7 trillion ($33.3 billion) allocated for development investment under the five-year financial plan.

The simultaneous launch of the five metro lines has therefore moved ahead of the financial framework needed to support them. While the investment scale has already been established, the mechanisms for generating revenue and mobilizing capital are still under development and have yet to receive approval from the Hanoi People’s Council.

According to draft resolutions submitted by the Hanoi People’s Committee, one notable proposal is to establish a mechanism for capturing the increase in land value generated by Transit-Oriented Development (TOD). Under the proposal, Hanoi would introduce new revenue sources from land value appreciation following planning adjustments, additional gross floor area created through higher development intensity, the commercial exploitation of railway infrastructure assets, infrastructure improvement charges, and public transportation connectivity fees. The model is intended to recover part of the value created by the metro system and reinvest it directly into transportation infrastructure.

At the same time, Hanoi has proposed diversifying its funding sources through the issuance of project bonds, infrastructure bonds, municipal bonds, and green bonds, alongside local government bonds permitted under current regulations. The city also plans to expand borrowing from credit institutions and the State treasury. These financing instruments are expected to provide additional medium and long-term funding capacity for large-scale infrastructure projects.

Attracting market capital

According to one capital markets expert, Hanoi’s plans to introduce financial instruments such as TOD value capture and various bond issuances represent necessary first steps but are only part of the equation. The decisive factor in attracting investment is not the number of financing tools available, but the quality of the projects themselves and the credibility of the financial structure presented to the market.

The expert noted that capital in financial markets is never in short supply; it simply flows toward investment opportunities that offer superior risk-adjusted returns. Investors do not commit funds simply because a project is large or strategically important. Rather, they evaluate each opportunity against competing investments across regional and global markets, weighing expected returns against potential risks before making a decision. The challenge, therefore, is not to “unlock” capital but to create investment opportunities compelling enough for capital to flow in naturally.

According to the expert, Vietnam’s large-scale infrastructure programs, including its urban railway system, are attracting growing interest from international investors. However, that interest remains largely exploratory because the information currently available is limited mainly to master plans, preliminary investment estimates, and implementation targets. Critical documents that investors rely on, including feasibility studies, financial plans, cash flow models, repayment strategies, and capital structures, have yet to be fully disclosed. Without this information, the market has no reliable basis for assessing either the project’s viability or its investment risks.

For any project seeking to raise funds in the capital market, a feasibility study is considered the single most important document. It must go beyond estimating total investment costs and answer fundamental questions: Who will the project serve? Where will its revenue come from? What cash flows will be used to repay debt? What assumptions underpin its financial projections? Investors also evaluate the quality of the project’s advisers, credit rating agencies, independent auditors, and other verification documents to assess the credibility of the financing package.

“Whether it is the central government, a local government, or a private company, any entity raising capital in the market is ultimately a borrower,” the expert said. “And every borrower must demonstrate how the funds will be used, how the debt will be repaid, and whether the project has been prepared professionally, transparently, and in accordance with standards accepted by the market.”

According to other industry experts, credibility in the capital market is not built through a single transaction but through consistently honoring commitments to investors. When project owners deliver projects on schedule, use capital for its intended purpose, and make principal and interest payments in full and on time, their creditworthiness gradually improves, lowering financing costs for future projects.

Conversely, if disclosures fail to accurately reflect reality or financial obligations are not fulfilled, market confidence will deteriorate, making future fundraising significantly more difficult.

As Hanoi prepares to implement one of the country’s largest metro investment programs, capital market specialists say investors are looking for more than new financing instruments. What the market needs is comprehensive, transparent information and a competitive financial plan capable of convincing both domestic and international investors.

Google translate

Google translate