Hanoi’s retail market has revolved largely around established commercial districts in the inner city for many years, particularly Hoan Kiem, where strong foot traffic, tourism activity, and limited supply helped sustain premium rents. But as the capital expands and consumer behavior evolves, retailers are increasingly reassessing where future growth lies.

That shift is becoming increasingly visible in Tay Ho Tay New Town. Japanese department store operator Takashimaya, best known in Vietnam for its flagship store at the Saigon Centre in Ho Chi Minh City, is expected to expand its Hanoi presence at Westlake Square Hanoi. The move reflects growing retailer interest in integrated urban districts that combine premium housing, office supply, hospitality, and long-term demographic growth.

According to the Hanoi Statistics Office, the total retail sales of goods and consumer services reached VND171.5 trillion ($6.6 billion) in the first two months of 2026, up 13.2 per cent year-on-year. Retail sales alone climbed 15.8 per cent to VND112.9 trillion ($4.3 billion), accounting for nearly two-thirds of total turnover and highlighting recovering domestic consumption and improving purchasing power.

But beneath the positive headline numbers, Hanoi’s retail property market is entering a more competitive and structurally-different phase, one increasingly defined by decentralization, experience-led retail formats, and intensifying competition among landlords as supply expands beyond the Central Business District (CBD).

Beyond the city center

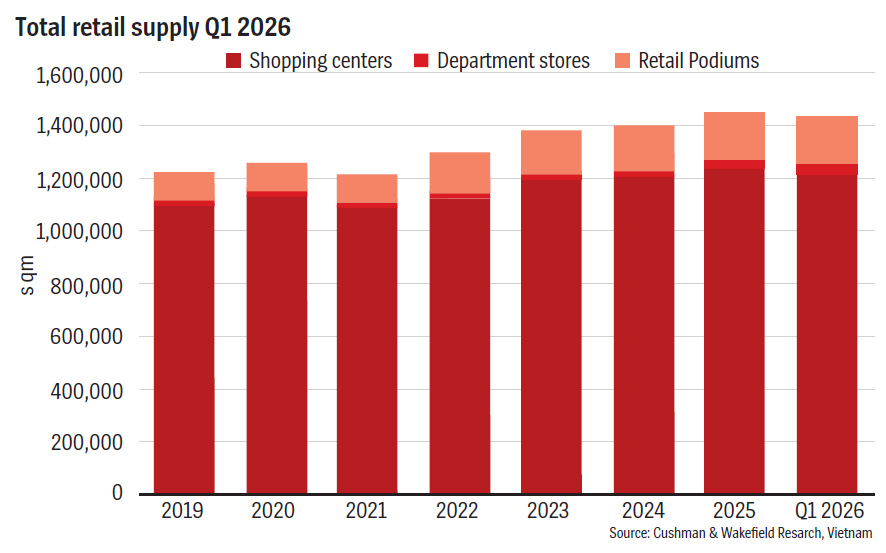

Hanoi’s retail geography is gradually being redrawn. According to the Hanoi MarketBeat Q1 2026 report from Cushman & Wakefield, Vietnam’s capital added 51,497 sq m of new retail space during the first quarter of 2026, bringing total retail stock to approximately 1.43 million sq m. The increase was driven primarily by the opening of the Hanoi Centre, a 50,000 sq m shopping center developed by Keppel in a secondary area, together with retail podium developments in western Hanoi. Shopping centers continue to dominate the market, accounting for around 85 per cent of total supply, underscoring the growing preference for larger, destination-style retail formats.

Crucially, most new supply is no longer concentrated in the traditional urban core. Cushman & Wakefield noted that developers are increasingly focusing on non-CBD districts, particularly western and suburban areas, where larger land plots and integrated township developments allow for more experiential retail concepts and stronger long-term catchment potential.

Between the remainder of 2026 and 2028, approximately 313,909 sq m of additional retail supply is expected to enter the market. Of that, suburban areas are projected to account for 153,500 sq m, while western Hanoi is expected to contribute 144,253 sq m, far outweighing future additions in central districts.

The broader direction of the market is echoed in the Savills Hanoi Q1/2026 Market Brief, which showed Hanoi’s modern retail stock reaching approximately 1.7 million sq m, with shopping centers remaining the dominant format and overall occupancy standing at 89 per cent. Savills observed that secondary districts and city-fringe areas are increasingly emerging as major retail destinations as Hanoi transitions toward a more decentralized, multi-center urban structure.

The consultants also linked this trend to Hanoi’s long-term urban planning strategy, which emphasizes suburban growth poles and satellite districts to relieve pressure on the city center. As land constraints continue to limit large-scale retail expansion in the CBD, growth is increasingly following new residential clusters and mixed-use urban developments.

Savills expects the supply wave to accelerate over the next several years. According to its report, nine projects are expected to add approximately 266,824 sq m of new retail space by the end of 2026. Between 2027 and 2028, much of the upcoming supply is projected to be concentrated in the Starlake area, where multiple projects are scheduled for completion within a relatively short timeframe.

This helps explain the growing appeal of areas such as Tay Ho Tay and Starlake. Once viewed primarily as residential expansion zones, these areas are evolving into mixed-use ecosystems combining office towers, embassies, hotels, research facilities, and premium housing - the type of concentrated environment increasingly favored by retailers seeking long-term footfall and higher-spending consumers.

The expected arrival of Takashimaya at Westlake Square Hanoi therefore appears less like an isolated investment and more like a reflection of a broader repositioning underway across Hanoi’s retail market.

Experience-led retail

According to the Hanoi MarketBeat Q1 2026 report, leasing activity during the first quarter continued to be driven primarily by food and beverage (F&B) and entertainment operators, helping absorb newly-completed retail space. Hanoi also saw the expansion of flagship retail concepts, including brands such as Phuc Long Dragon and Skechers, reinforcing retailer confidence despite intensifying competition.

Developers, in turn, are increasingly adjusting their strategies to reflect changing consumption habits. Cushman & Wakefield noted that landlords are placing greater emphasis on tenant mix optimization, experiential retail concepts, and community-oriented spaces to sustain visitor traffic and improve long-term occupancy stability. Rather than functioning solely as shopping destinations, malls are increasingly being positioned as places where consumers can dine, socialize, and spend leisure time.

A broader regional perspective reinforces the trend. In its “Retail in Motion: Turning Global Signals into Strategic Considerations” report, Cushman & Wakefield identified “experience-led demand” as one of the defining characteristics shaping retail markets across Asia. Rather than operating purely as retail venues, shopping centers are increasingly functioning as “third places” - environments for gatherings, recreation, and lifestyle experiences. Across regional markets, categories such as F&B, wellness, entertainment, and hybrid lifestyle concepts are increasingly outperforming traditional fashion-led retail models.

Savills similarly observed that future large-scale developments in Hanoi are likely to place greater emphasis on differentiation and consumer experience as competition intensifies, particularly in emerging suburban districts where retail destinations are still being established.

This transition is also reshaping how retailers evaluate locations. Increasingly, brands are prioritizing districts with stronger residential density, integrated infrastructure, and long-term demographic growth over purely historic centrality.

Stronger competition

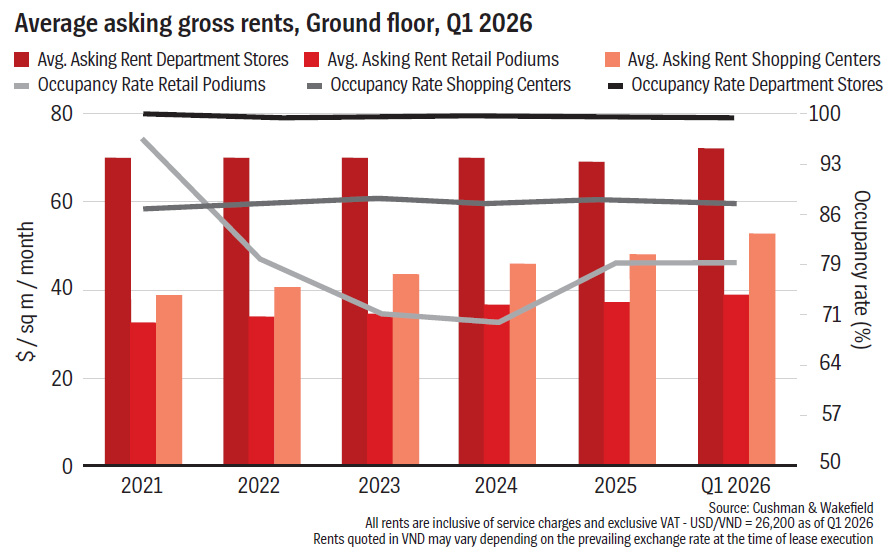

Even as Hanoi’s retail market expands, developers are entering a more demanding environment. According to Cushman & Wakefield, average occupancy stood at 86.5 per cent during the first quarter, increasing 1.1 percentage points year-on-year but down slightly quarter-on-quarter as newly-completed projects entered lease-up phases and some tenants remained in fit-out periods. At the same time, average ground-floor asking rents climbed to $51.4 per sq m per month, rising 9.1 per cent quarter-on-quarter and 10.1 per cent year-on-year.

The increase in rents was driven partly by newly-launched projects in secondary districts entering the market at higher asking levels than older stock. Leasing demand in prime locations also remained resilient, particularly for professionally-managed schemes with strong branding and visibility, according to Cushman & Wakefield.

Savills likewise reported continued rental resilience, with market rents increasing 4 per cent year-on-year, despite the growing supply pipeline. The consultants noted that shopping centers continue to outperform other retail formats due to stronger operational quality and their ability to adapt to evolving consumer preferences.

At the same time, future supply growth is likely to intensify competition among landlords, particularly in non-CBD districts where the majority of new projects are concentrated. Cushman & Wakefield expects longer lease-up periods and greater leasing flexibility to become increasingly necessary as projects compete for tenants and footfall. Developers with stronger residential catchments, clearer positioning, curated tenant ecosystems, and destination-oriented retail concepts are expected to outperform in the next stage of market growth.

For Hanoi, the rise of developments such as Westlake Square Hanoi may ultimately represent something larger than a single commercial project. It signals the emergence of a retail landscape no longer centered solely around the traditional CBD, but increasingly shaped by a network of new urban hubs where retail, lifestyle, and residential demand converge.

Google translate

Google translate