Over the past three decades, Vietnam’s merger and acquisition (M&A) market has undergone successive cycles of expansion, correction, and recovery, mirroring the country’s broader economic transformation. Unlike many regional markets, M&A activity in Vietnam has rarely been driven by investor sentiment alone. Rather, deal activity has often been shaped by structural factors such as policy direction, access to capital, market development, regulatory openness, and the transaction capabilities of businesses and investors.

These underlying dynamics were the focus of the recent Venture Forum 2026 in Ho Chi Minh City, with the theme “Vietnam’s M&A Moment - The Unseen Dynamics,” where investors, industry experts, businesses, and innovation support organizations discussed the outlook for Vietnam’s M&A market, emerging investment trends, growth and exit strategies, and opportunities within the country’s innovation-driven economy.

Shift in momentum

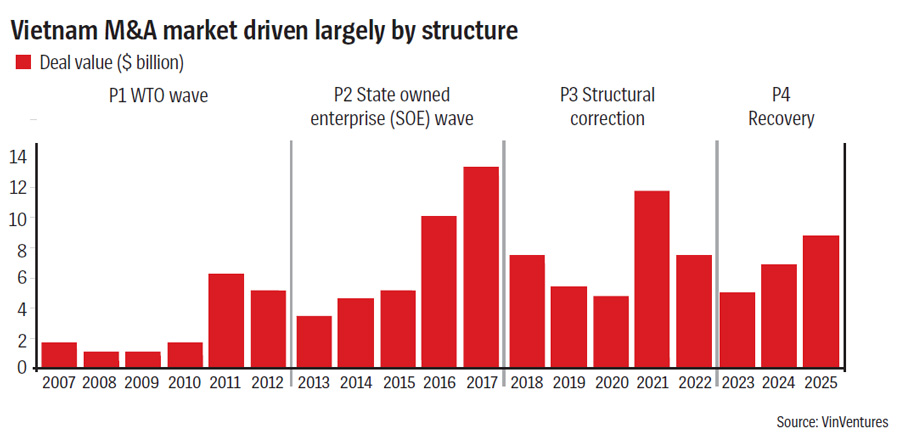

According to a VinVentures survey released at the Forum, capital flows into Vietnam’s M&A market over the past 12 years have shown a clear pattern, with most transactions continuing to be concentrated in the real economy, including real estate, consumer goods, industrials, and sectors closely linked to the country’s economic growth.

This trend reflects the characteristics of Vietnam’s development model, where capital has consistently gravitated toward sectors with scale, strong market demand, operational depth, and clearer transaction pathways. The report identified 2022 as a pivotal turning point, when the market entered a correction phase as three factors simultaneously tightened deal-making conditions.

First, the corporate bond market contracted sharply, reducing a key source of financing for M&A transactions.

Second, foreign investor participation became more constrained, making cross-border deals more difficult to execute.

And third, the valuation gap between buyers and sellers widened significantly. While Vietnamese companies continued to be valued at around 16.5-times earnings, buyers were willing to pay only about eleven-times.

As a result, many transactions became harder to finance, more difficult to price, and increasingly challenging to complete. However, the subsequent recovery also underscored the growing importance of domestic capital. The share of local investors rose from 16 per cent to 46 per cent of total deal value, indicating that Vietnam’s M&A market is no longer reliant solely on foreign capital. The 2022 correction revealed three key market signals.

The first is the rise of the technology sector. Though technology accounted for only around 15.9 per cent of total deal value, the figure should not be viewed as a growth ceiling. Rather, it reflects a market that is still maturing, where exit pathways remain under development.

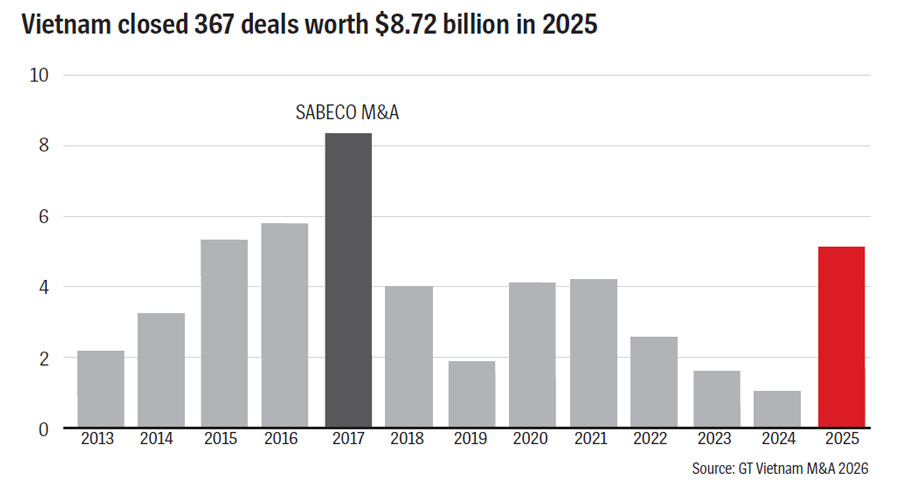

The second is the significance of the 2017 benchmark. According to VinVentures, approximately 58 per cent of total deal value that year came from the landmark SABECO transaction. Excluding this outlier, the current market size is, in fact, much closer to its historical peak than headline figures suggest.

And the third is the growing strength of domestic capital. Over the past 12 years, local investors have accounted for an average of around 35 per cent of total deal value, demonstrating that domestic capital is not merely a temporary support factor but a structural component of Vietnam’s M&A landscape.

Notably, while technology still represents a relatively modest share of total deal value, its presence has been increasing steadily over time. Though the sector has yet to dominate headline transactions, the trend is clearly reflected in market data.

Combining historical patterns with Vietnam’s current market conditions leads to a consistent conclusion: the country’s M&A market still has significant room to expand in terms of scale, depth, and activity.

As Ms. Le Han Tue Lam, CEO of VinVentures, pointed out, these signals suggest that Vietnam’s M&A market should not be assessed solely against past peaks or foreign investor sentiment. Instead, it should be viewed through the lens of technological advancement, the growing strength of domestic capital, and an increasingly balanced and diversified transaction base. “From our perspective, the more important question is not when the market moves, but why it moves,” she said. “This is a market where capital only flows when the right conditions are in place.”

Therefore, VinVentures believes that Vietnam’s M&A market should be evaluated not only through investor sentiment but also through the underlying conditions that enable capital to move, including policy direction, access to financing, market infrastructure, and regulatory openness.

From the perspective of a foreign investor, Mr. JunSung Bae, Executive Director of the Investment Division at Lotte Ventures, said Vietnam is emerging as one of Southeast Asia’s most dynamic markets, underpinned by strong economic growth, a young population, and a rapidly-evolving innovation ecosystem.

International investors, he continued, are drawn not only by Vietnam’s growth momentum but also by the quality of its startup ecosystem, entrepreneurial spirit, and the ambition of Vietnamese founders to address global challenges. “We believe that when this innovative energy is combined with the industrial infrastructure and business platforms of large corporations, Vietnam can unlock significant opportunities for growth and innovation in the years ahead,” he said.

Lotte Ventures - the corporate venture capital arm of South Korea’s Lotte Group - has made more than 300 investments globally, in South Korea, Vietnam, Silicon Valley in the US, and Japan. In Vietnam, it is expanding its investment activities through L-CAMP Vietnam, an accelerator program that connects local startups with Lotte Group affiliates, South Korean corporations, and global partners through business collaboration and proof-of-concept opportunities.

Domestic capital on the rise

Vietnam’s position within the regional and global investment landscape continues to strengthen, attracting growing interest from both strategic and financial investors. At the same time, shifting capital flows are creating new opportunities across sectors and shaping the next phase of the country’s M&A market. However, investors argue that unlocking the market’s full potential will require progress on several longstanding challenges, particularly valuation, exit pathways, and corporate governance.

Mr. Chris Freund, Founder and Managing Partner of Mekong Capital, highlighted the growing presence of family offices in Vietnam as one of the market’s most notable developments in recent years. He added that these organizations are becoming increasingly professionalized and are emerging as a new source of capital for M&A transactions. “Nowadays, domestic family offices are among the potential buyers in most transactions taking place in Vietnam,” he said.

However, the valuations domestic investors are willing to pay often fall below sellers’ expectations, limiting their appeal in many deals. Nevertheless, the rise of domestic capital is seen as a positive development, helping reduce the market’s reliance on foreign funding and enhancing its resilience to global economic volatility.

Domestic family offices are now among the potential buyers in most M&A transactions taking place in Vietnam. These organizations are becoming increasingly professionalized and are emerging as a new source of capital for the country’s M&A market.

Mr. Andrea Campagnoli, Founding Partner at Bain Vietnam, said the higher global interest rate environment has significantly increased the cost of capital, prompting investment funds to recalibrate their return expectations. “Many international investors are currently targeting internal rates of return (IRR) of around 15-18 per cent for investments in Asia,” he said.

Meanwhile, many Vietnamese businesses continue to benchmark their valuation expectations against the market’s previous high-growth period. The widening gap between buyers’ and sellers’ expectations has become one of the main reasons why transactions are taking longer to complete or failing to close altogether. According to experts, this is not unique to Vietnam but reflects a broader global trend. However, the challenge is more pronounced in emerging markets such as Vietnam, where exit channels remain relatively limited.

Mr. Tze Hoe Chan, Managing Partner of ZIDO Capital Asia, argued that a healthy M&A market requires a more diversified exit ecosystem. “M&A is an important exit channel, but it cannot be the only one,” he said. “The quality of the IPO market plays a decisive role in attracting private capital.” In his view, more effective and diversified exit options would provide investors with greater flexibility to realize returns, thereby encouraging fresh capital inflows.

Vietnam’s potential stock market upgrade could improve liquidity, increase institutional investor participation, and establish more transparent valuation benchmarks for M&A transactions. Another recurring theme throughout the discussions was the growing importance of corporate governance in determining deal success.

According to Mr. Freund, companies with professional Boards of Directors, strong management teams, and transparent governance structures are significantly more attractive to investors. “Businesses with capable boards, strong CEOs, and solid management teams are much easier to sell,” he explained. “By contrast, companies that remain overly dependent on their founders often face greater challenges during the exit process.”

Drawing on Mekong Capital’s investment experience, Mr. Freund cited pharmacy chain Pharmacity as an example. Five years ago, the company faced significant challenges related to merchandising and supply chain management. Following operational restructuring, same-store sales increased by approximately 35 per cent annually, while pharmaceutical sales doubled within two years. According to Mr. Freund, the case demonstrates how improvements in governance and operations can directly enhance a company’s value.

Beyond traditional sectors such as real estate, consumer goods, and industrials, investors also see strong potential in emerging technology sectors. Mr. Freund said Mekong Capital is paying close attention to opportunities in biotechnology and agricultural technology, and noted that Vietnam’s growing pool of scientific and technical talent provides a solid foundation for the development of higher value-added industries. One company in Mekong Capital’s portfolio has become the world’s largest producer of insect protein and the lowest-cost player in the industry.

As AI, biotechnology, and digital transformation continue to reshape industries, companies with proprietary technologies and strong innovation capabilities are likely to become the focus of the next wave of M&A activity.

Despite ongoing challenges, investors agreed that Vietnam possesses strong fundamentals to enter a new phase of M&A growth. However, unlocking this potential will require continued efforts to improve the regulatory framework, strengthen corporate governance standards, expand exit channels, and build a more transparent and efficient investment ecosystem.

Outlook to 2030

According to the VinVentures report, Vietnam’s M&A market could reach $14-16 billion by 2030, based on a three-scenario model and two independent forecasting methods that converge within the same range. The outlook is underpinned by several structural factors.

First, after excluding the one-off impact of the SABECO transaction, the market’s current trajectory suggests that Vietnam’s M&A landscape has remained fundamentally resilient rather than purely cyclical.

Second, three distinct sources of deal supply are expected to converge simultaneously: State-owned enterprise (SOE) divestments, mounting exit pressure from private equity funds approaching the end of their investment cycles, and founders seeking succession plans, strategic partnerships, or partial exits.

Finally, both historical precedents and current market conditions point to the same growth trajectory, reinforcing confidence in the market’s long-term potential.

“Combining historical patterns with Vietnam’s current market conditions leads to a consistent conclusion: the country’s M&A market still has significant room to expand in terms of scale, depth, and activity,” Ms. Lam said.

However, she stressed that the key message is not merely about transaction value but about market maturity. “Vietnam is entering this next phase with stronger liquidity, clearer exit pathways, more visible deal supply, and a growing domestic capital base,” she said.

These conditions suggest that M&A can evolve beyond a transaction tool to become a mechanism for corporate growth, capital recycling, technology adoption, and ecosystem development. For investors, founders, and corporates, the opportunity lies not only in participating in the next growth cycle but also in helping shape a more mature and dynamic M&A market in Vietnam.

We believe that when the quality of its startup ecosystem is combined with the industrial infrastructure and business platforms of large corporations, Vietnam can unlock significant opportunities for growth and innovation in the years ahead.”

Google translate

Google translate