Vietnam’s long-term retail outlook continues to strengthen despite an increasingly uncertain global economic environment. Backed by resilient domestic demand, supportive government policies, and a rapidly-expanding digital economy, the country is positioning itself as one of Southeast Asia’s most attractive consumer markets for both domestic and international retailers.

Yet beneath those encouraging fundamentals, the rules of retail are changing. Consumers are becoming more selective, shopping journeys are increasingly fragmented across physical and digital channels, and AI is reshaping everything from product discovery to pricing and customer engagement. Growth alone is no longer enough to guarantee success.

Insights shared by industry leaders at the “Vietnam Retail Decoded: Trade, Growth and Market Entry” business seminar, held recently by Acclime Vietnam, suggest that the country’s next retail winners will not simply be those that invest the most, but those that best understand how Vietnamese consumers are evolving. The discussion highlighted how shifting consumer behavior, omnichannel retail, and AI are reshaping one of Asia’s fastest-changing consumer markets.

Succeeding in the retail boom

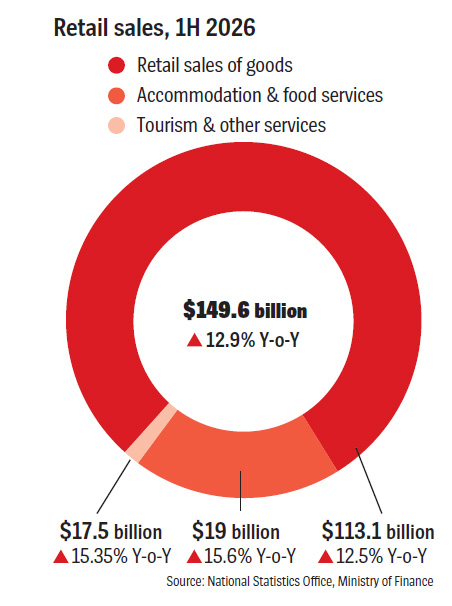

According to Mr. Vlad Savin, Partner at Acclime Vietnam, Vietnam aims to increase total retail sales of consumer goods and services from approximately $270 billion in 2025 to nearly $450 billion by 2030. The scale of that expansion represents a significant opportunity for both established retailers and new entrants looking to gain a foothold in one of Asia’s fastest-growing consumer markets. “The opportunity over the next five years is significant for both existing businesses and future investors entering Vietnam,” he said.

Much of that growth will be driven by the country’s digital transformation. Vietnam expects the digital economy to contribute around 30 per cent of GDP by 2030; more than doubling its estimated 14 per cent share in 2025. Retail and e-commerce are expected to play a central role in that transition, gradually emerging alongside manufacturing as one of Vietnam’s key economic growth engines.

The opportunity over the next five years is significant for both existing businesses and future investors entering Vietnam.

Supporting that momentum is a series of government measures aimed at stimulating domestic consumption and encouraging investment. Recent policies include maintaining the reduced value-added tax rate, increasing personal income tax deductions, and introducing incentives for small and medium-sized enterprises, including a two-year corporate income tax holiday for qualifying businesses.

The market’s strong fundamentals continue to attract investment. International brands are steadily expanding their presence in Vietnam through both physical stores and digital channels, while merger and acquisition activity remains vibrant as companies compete for market share in an increasingly dynamic retail landscape.

Nowhere is that momentum more evident than in e-commerce. Vietnam has rapidly climbed the regional rankings to become Southeast Asia’s third-largest e-commerce market by gross merchandise value, behind only Indonesia and Thailand. Just five or six years ago, the country ranked fifth or sixth in the region. “Based on the current trajectory, Vietnam is well-positioned to become the region’s second-largest e-commerce market by 2030,” Mr. Savin believes.

Yet he cautioned that market growth alone does not guarantee success. As competition intensifies and the retail landscape continues to evolve, businesses will need more than capital to succeed. Understanding changing consumer behavior, selecting the right market entry strategy, and building for long-term growth will increasingly determine which brands emerge as winners in Vietnam’s next retail chapter.

Trust the new currency

Vietnam’s strong retail outlook masks a more cautious reality at the household level. While economic growth has remained resilient, consumers are becoming increasingly selective about how and where they spend their money; a shift that may prove just as significant for retailers as the market’s headline growth projections.

According to Mr. Peter Christou, General Manager of Worldpanel by Numerator, Vietnam’s economy maintained solid momentum through 2025, with GDP growing by around 8 per cent as household incomes continued to improve. However, first-party purchasing data collected directly from Vietnamese households suggests consumer confidence has become increasingly fragile.

Concerns over food safety, household income, job security, and rising utility costs have all intensified over the past year, influencing not only how much consumers spend but also how they evaluate purchases. “When people are worried about their income or their financial security, it changes the way they think about spending money,” Mr. Christou said.

The shift reflects the cumulative impact of several challenging years. Following the Covid-19 pandemic, households have also faced inflationary pressures, global economic uncertainty, and a series of high-profile food safety scandals that have eroded confidence in certain products.

For brands, rebuilding that confidence is becoming just as important as competing on price. “Trust is the new currency,” Mr. Christou said. The changing mindset is particularly evident in the fast-moving consumer goods (FMCG) segment.

For several years, manufacturers were able to offset weaker sales volumes through higher prices. That strategy is becoming increasingly difficult as consumers grow more deliberate in their purchasing decisions. Across many FMCG categories, price increases are no longer sufficient to compensate for declining consumption volumes.

The pressure is most visible in food and beverage categories such as dairy, packaged foods, and beverages, while personal care and home care products have remained comparatively resilient. “There isn’t a one-size-fits-all story,” Mr. Christou said. “Some categories continue to grow strongly while others remain under pressure.” The strongest performers tend to be products that address changing lifestyles, particularly those centered on convenience, health, and everyday practicality.

At the same time, spending patterns continue to evolve. The recovery of domestic and international tourism has supported restaurants, cafés, and foodservice businesses, illustrating that consumers are not necessarily spending less but are becoming more intentional about where they spend.

For retailers, that distinction is critical. Growth can no longer be taken for granted simply because Vietnam’s consumer market is expanding. Increasingly, success depends on understanding what motivates purchasing decisions and earning consumer trust in an environment where shoppers have become more informed, more selective, and less willing to spend without confidence.

One country, many consumer markets

One of the biggest mistakes brands can make when entering Vietnam is assuming they are entering a single consumer market. In reality, the country’s 100 million consumers represent a diverse and increasingly fragmented landscape shaped by regional differences, income disparities, changing household structures, and evolving lifestyles. Strategies that succeed in one region, or with one consumer segment, may struggle to gain traction elsewhere.

Mr. Christou said companies should move beyond viewing Vietnam as a homogeneous market and instead identify distinct consumer clusters with different needs and purchasing behaviors. “Vietnam is a very long country,” he said. “Between the northern, central, and southern regions, behaviors and culture can be very different.”

Income distribution illustrates that complexity. While Vietnam’s growing middle class continues to attract international retailers, purchasing power remains uneven. Around 18 per cent of households earn VND6 million ($231) or less per month, while only about 7 per cent earn more than VND30 million ($1,154). Those differences influence everything from pricing strategies and product positioning to retail channel selection. “It’s easy to forget that when we live in Ho Chi Minh City,” Mr. Christou said. “But that’s the reality of consumers around the country.”

At the same time, Vietnam’s household structure is changing. Households with three or fewer members now account for nearly half of all households nationwide, representing around 13.5 million households. As urbanization and demographic trends reshape family life, smaller households are becoming one of the country’s most influential consumer segments.

For brands, the implications extend well beyond household size. Smaller households typically spend more on a per-person basis, place greater emphasis on convenience and self-care, and are more willing to pay for products that save time or improve everyday lifestyles. As birth rates decline, rising pet ownership is also creating new opportunities across pet food and related services.

Consumer preferences are evolving just as quickly. Vietnam’s FMCG market now sees more than 35 new product launches every day, yet innovation alone is no longer enough to guarantee success. “The innovation part is easy,” Mr. Christou said. “The sustaining part is the challenge.”

Only a small proportion of new products achieve meaningful household penetration, highlighting how difficult it has become to maintain relevance in a market where consumers are constantly exposed to new alternatives.

As a result, brands are placing greater emphasis on understanding why consumers buy rather than simply what they buy. Products that align with specific consumption occasions, whether centered on convenience, health, indulgence or energy, are increasingly outperforming those relying solely on traditional category positioning.

For retailers, the message is clear. Vietnam’s retail opportunity is no longer defined simply by rising incomes or expanding consumption. It is shaped by increasingly diverse consumer segments with different expectations, spending priorities, and lifestyles. Understanding those differences is becoming just as important as understanding the market itself.

New retail battlefield

As Vietnam’s consumer landscape becomes increasingly fragmented, so too are the channels through which consumers shop. Success is no longer determined simply by securing shelf space in supermarkets or launching an online store. Instead, brands are competing in a marketplace where consumers move seamlessly between neighborhood shops, convenience stores, supermarkets, e-commerce platforms, and social commerce, often within the same purchasing journey.

According to Mr. Christou, that shift requires retailers to fundamentally rethink how they define growth. “Winning shoppers is the most important factor,” he said. “Around 80 per cent of the people who bought your brand this year won’t necessarily buy it again next year.”

For decades, retailers have focused on building customer loyalty. Mr. Christou believes that approach is becoming less effective in today’s Vietnam. Rather than relying on repeat purchases from existing customers, brands should focus on continuously attracting and re-engaging shoppers. “We shouldn’t chase loyalty,” he said. “We should focus on winning shoppers and re-winning shoppers.”

The reason lies in how Vietnamese consumers now shop. New products, promotions, and online trends spread rapidly, making consumers more willing than ever to experiment with different brands. The same shopper who tries a new product today may switch to another tomorrow, making relevance more valuable than familiarity.

That behavior is also reshaping retail channels. Traditional trade continues to dominate Vietnam’s FMCG market, particularly outside major cities, while supermarkets, convenience stores, and mini-marts continue expanding into secondary cities and rural areas. At the same time, online grocery shopping has become mainstream, with around 70 per cent of urban households and nearly half of rural households now purchasing FMCG products online at least once a year.

Rather than replacing physical retail, e-commerce has become another step in the purchasing journey. Consumers may discover products on social media, compare prices across marketplaces, visit a store to examine an item before purchasing online, or do the reverse. Increasingly, shopping is no longer confined to a single channel. “The consumer wants the same seamless experience whether they’re shopping online or offline,” Mr. Christou said. That evolution is accelerating the shift from multichannel to true omnichannel retail, where physical and digital touchpoints function as a single ecosystem.

For new market entrants, digital platforms often provide the fastest path to consumers. Without competing for limited shelf space in traditional retail, brands can establish an online presence more quickly while recommendation algorithms and targeted marketing improve product visibility.

Yet online and offline should not be viewed as competing channels. Rather, they complement one another, allowing consumers to discover, compare, and purchase products whenever and wherever it is most convenient.

The rapid rise of TikTok Shop illustrates how quickly competitive dynamics can change. While Shopee and Lazada established their presence years earlier, TikTok Shop has rapidly expanded its customer base by focusing on acquiring new shoppers rather than relying primarily on existing users. The strategy reflects a broader reality across Vietnam’s retail market.

Consumers are making fewer shopping trips overall, but they are visiting more retailers and comparing more platforms before making a purchase. “They have accounts everywhere,” Mr. Christou said. “They’ll compare prices and choose whichever platform offers the best value at that particular moment.”

For brands, that means availability has become a competitive advantage in itself. If consumers regularly shop across six or seven different channels while a product is available in only one, the opportunity to influence purchasing decisions is immediately reduced.

Winning in Vietnam’s increasingly fragmented retail landscape therefore depends less on retaining yesterday’s customers than on continually earning tomorrow’s shoppers. Brands that understand where consumers shop, why they choose different channels and how those channels work together will be far better positioned to compete as the market continues to evolve.

AI reshapes retail

AI has rapidly become one of the defining forces in modern retail, influencing everything from product discovery and pricing to marketing and inventory management. Yet despite the excitement surrounding AI, its greatest impact may not be replacing human decision-making, but improving how consumers and businesses make decisions.

Mr. Christou believes much of the discussion around AI overstates its role in consumer purchasing. “I don’t believe we’re yet at the point where AI is making purchasing decisions on behalf of consumers,” he said. “What AI is doing is helping people make better-informed decisions.”

Across digital marketplaces, AI-powered recommendation engines are already shaping how consumers discover products by analyzing browsing behavior, previous purchases, and individual preferences. Mr. Christou attributes much of TikTok Shop’s rapid growth to the strength of its recommendation algorithm, which has transformed product discovery from traditional search into personalized content recommendations.

AI is also making it easier for shoppers to compare products, evaluate reviews, and assess value before making a purchase. “Consumers are still making their own decisions,” Mr. Christou said. “AI is helping them understand what’s available.”

While consumers experience AI through more personalized shopping journeys, retailers are increasingly using it to improve operations. According to Mr. Ryan Vo, Senior Account Manager at Amazon Global Selling Vietnam, AI is streamlining many of the tasks traditionally associated with cross-border e-commerce, helping Vietnamese businesses expand internationally more efficiently.

AI-powered tools can now generate and optimize product listings, improve multilingual content, and adapt product information for different international markets, reducing one of the biggest barriers facing Vietnamese exporters.

The technology is also helping businesses navigate regulatory requirements by monitoring certification and compliance obligations across multiple marketplaces, while AI-assisted advertising tools analyze campaign performance and recommend ways to improve conversion rates and marketing efficiency.

Perhaps most importantly, AI is enabling retailers to make more informed strategic decisions. By analyzing customer behavior and demand patterns, businesses can identify emerging market opportunities and better determine which products are most likely to succeed in different countries.

“The operational impact is already becoming measurable,” Mr. Vo said, noting that many routine tasks previously handled manually can now be automated, allowing smaller teams to manage international e-commerce operations while focusing on brand development and long-term growth.

Ultimately, AI is enhancing both sides of the retail equation. For consumers, it delivers more personalized and informed shopping experiences. For retailers, it improves efficiency, strengthens compliance and supports faster international expansion. In both cases, however, human judgment remains central. AI is not replacing decision-making, it is making better decisions possible.

Winning the next chapter

Vietnam’s retail market may be expanding rapidly, but long-term success will depend on execution rather than opportunity alone. For businesses entering the market, choosing the right growth strategy begins long before the first product reaches consumers.

Mr. Savin said companies should carefully evaluate their market-entry approach from the outset, whether establishing a local entity, entering through cross-border e-commerce or adopting a phased expansion strategy. Those early decisions can have lasting implications for licensing, taxation, future investment, and business scalability.

“We need to understand what model makes sense today, but also what happens in the next two or three years,” he said. “Whether a company plans to expand, attract investment, or pursue an acquisition later, those decisions should be considered from the outset.”

Operational readiness is equally critical. According to Mr. Nguyen Viet Hung, Deputy Director of VietinBank, businesses should establish robust financial and compliance systems from Day 1. Proper capital structuring, integrated payment systems, and disciplined cash flow management not only improve operational efficiency but also minimize regulatory risks as companies expand.

Profit repatriation, tax compliance, and transaction management should be treated as strategic priorities rather than administrative requirements, particularly as Vietnam continues strengthening financial transparency and regulatory oversight.

Yet strategy and operations alone will not determine success. Consumers are becoming more informed, more connected and more selective. They expect seamless experiences across physical and digital channels, compare products and prices more easily than ever before, and are increasingly willing to switch brands in search of better value or greater convenience.

For retailers, that means competitive advantage is no longer built solely on scale or price. It is built on understanding consumers more deeply, responding more quickly to changing shopping behaviors, and using technology to improve every stage of the customer journey.

Vietnam’s retail market is expected to become larger over the coming decade. Competition will become more intense. The companies that emerge as leaders are unlikely to be those that simply invest the most or enter the market first. They will be those that evolve as quickly as Vietnam’s consumers do.

At a glance: Vietnam’s retail market in 2026

Major retailers expanding

- Central Retail: $1.38-1.44 billion in investment, targeting 330+ stores by 2027;

- AEON: $1.5 billion in investment, aiming to triple its scale by 2030;

- WinCommerce: Targeting 10,000 stores by 2030.

Foreign brands continue to enter Vietnam

Recent international entrants include: POP MART; Oh!Some; MR.DIY; KKV; and Flying Tiger Copenhagen.

M&A momentum

In the first five months of 2026, the wholesale and retail sector ranked first in inbound merger and acquisition activity, accounting for 45.4 per cent of total capital contributions and share acquisition transactions. (Source: Acclime Vietnam)

Google translate

Google translate