Vietnam’s economy continued to sustain a broad-based recovery in the first four months of 2026, with positive signs coming from industrial production, investment, and international goods trade. Alongside this growth momentum, however, inflationary pressures have risen rapidly, input costs have climbed, the trade deficit has widened, and structural risks, particularly dependence on the FDI sector, are becoming increasingly evident constraints on the economy’s goal of achieving high and sustainable growth.

Industrial production remains resilient

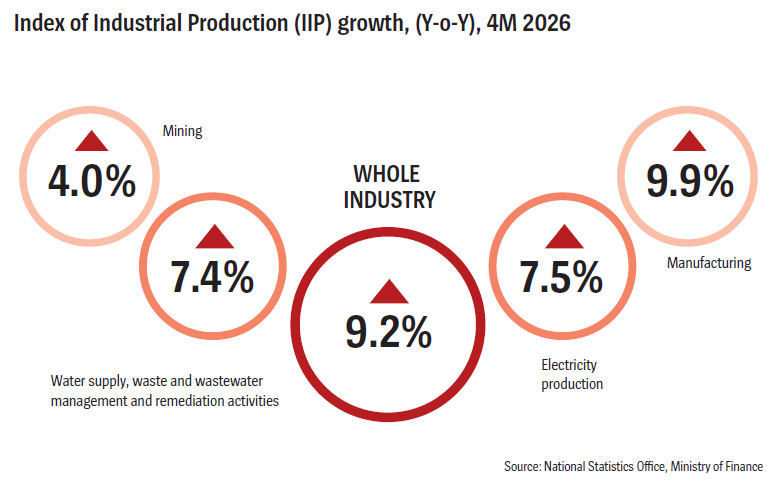

One bright spot in the economic picture for the first four months was that industrial production maintained solid growth. The Index of Industrial Production (IIP) rose 9.2 per cent, up 0.6 percentage points against the same period last year. Within this, manufacturing and processing, the main driver of growth, expanded 9.9 per cent.

However, behind these impressive figures are signs suggesting that production momentum is beginning to slow. Growth in manufacturing and processing was 0.7 percentage points lower than in the same period last year, indicating that the sector’s rebound is not as strong as in earlier phases.

The April 2026 Purchasing Managers’ Index (PMI) further reinforced this assessment, declining to 50.5 points; close to the contraction threshold. Notably, new orders fell for the first time in eight months, while the pace of output growth slowed significantly.

One major concern is that input costs have risen at the fastest rate in 15 years, driven primarily by higher fuel, oil, and transportation costs amid geopolitical instability in the Middle East. To offset these pressures, companies have been forced to raise selling prices, resulting in the fastest increase in output prices since 2011.

This indicates that the production sector is being “squeezed” from both ends, with rising costs and weakening demand. As higher output prices dampen consumer demand, the cost-price spiral could become a significant drag on growth in the months ahead. While production continues to expand in scale, growth momentum is clearly weakening under pressure from rising costs and softening market demand.

Inflation accelerates

Consumer price developments in the first four months show that inflationary pressures are rising faster than expected. The CPI in April increased 5.46 per cent year-on-year, bringing the CPI for the four-month period to 3.99 per cent. This increase, in the context of simultaneously rising input and output prices, suggests that inflationary pressure for 2026 as a whole will be substantial. The target of keeping inflation at around 4.5-5 per cent is facing considerable challenges.

Unlike previous periods, current inflation is strongly characterized by cost-push factors. Higher fuel prices, raw material costs, and logistics expenses have affected multiple sectors, pushing up the overall price level across the economy.

Meanwhile, monetary policy space is becoming increasingly limited, as policymakers must balance inflation control with growth support. Without flexible and timely management, inflation could quickly become the most significant constraint on macro-economic policy in the months ahead. Inflation is no longer a latent risk but an immediate pressure, directly narrowing both monetary and fiscal policy space.

Businesses rise & Institutional reform

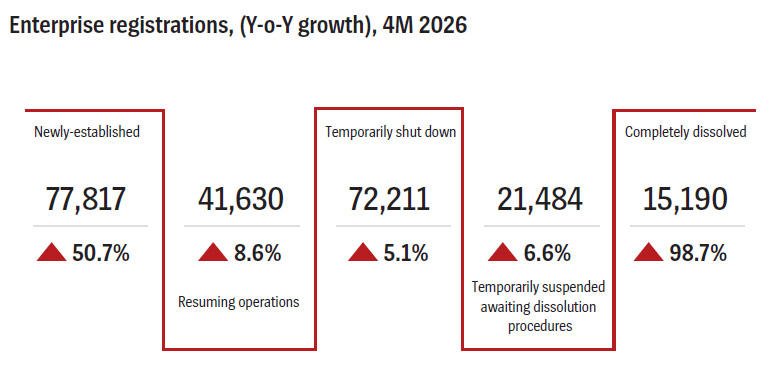

Some 119,400 enterprises entered the market in the first four months of the year, including 77,800 newly-established enterprises and 41,600 resuming operations. This is a positive sign, reflecting an initial improvement in business confidence.

On the other hand, the number of enterprises exiting the market remained high, at 108,900. The exit rate was equivalent to 91.2 per cent of total new entries, indicating that the business environment remains challenging, particularly amid rising input costs, weak demand, and limited corporate resilience.

The structure of newly-established enterprises continued to be heavily skewed toward consumer service sectors, while productive capacity has not improved proportionally. Though business activity is becoming more dynamic in terms of quantity, quality and durability remain persistent weaknesses. This poses a barrier to improving the quality of economic growth over the medium and long term.

A notable institutional highlight in the first four months was the government’s issuance of eight resolutions aimed at cutting and simplifying administrative procedures and business conditions on an unprecedented scale. The removal of 184 administrative procedures and 890 business conditions, if effectively implemented, could reduce compliance time and costs for businesses by more than 50 per cent. This sends a strong signal of commitment to reform, helping to reinforce confidence among businesses and investors.

However, the issue is not only how much is cut but whether these reductions are substantive or merely procedural shifts. The effectiveness of reform will depend on decentralization, accountability, and implementation capacity. Institutional reform will only deliver real impact if it goes beyond reducing the number of procedures and conditions and ensures meaningful changes in practice.

Public investment & Strong FDI inflows

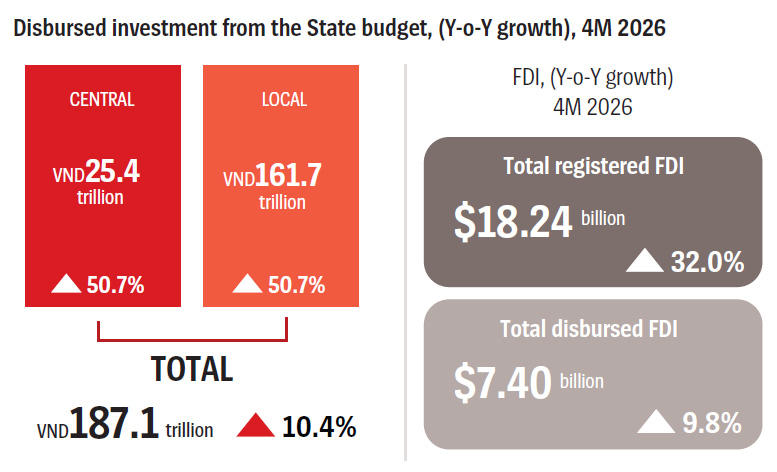

Public investment disbursement in the first four months reached VND187.1 trillion ($7.2 billion), equivalent to 19.7 per cent of the annual plan and up 10.4 per cent year-on-year. This represents solid progress, contributing to growth support amid ongoing difficulties in the private sector.

Public investment continues to play a leading role as the economy requires stimulus. However, its spillover effects appear to be weakening. Specifically, each VND1 of public investment in 2024 leveraged VND3.12 from the non-State sector and VND0.92 from the FDI sector, while these figures declined to VND2.63 and VND0.80, respectively, in 2025.

The diminishing ability of public investment to draw in capital from the private and FDI sectors suggests that links and spillover effects across economic sectors have not improved significantly.

FDI inflows continued to be a bright spot in the first four months of 2026. Total registered FDI stood at $18.24 billion, up 32 per cent year-on-year. Notably, the average size of newly-licensed projects rose sharply, to $9.7 million, while disbursed FDI reached $7.4 billion; the highest level in five years and reflecting sustained confidence among foreign investors in Vietnam’s investment environment.

However, a closer look at the structure of FDI reveals a noteworthy trend: a shift from greenfield investment toward acquisitions of existing assets. Of total registered capital, as much as $2.96 billion came from capital contributions and share purchases, up 61.9 per cent year-on-year. Notably, foreign investor purchases of domestic shares that did not increase charter capital reached $2.51 billion, accounting for 13.76 per cent of total registered FDI and 2.57-times higher than in the same period of 2025. This suggests that a significant portion of FDI inflows do not create new productive capacity but instead reflect transfers of ownership of existing domestic enterprises and assets.

This development reflects two sides of the same coin. On the positive side, the increase in merger and acquisition (M&A) activity indicates that Vietnam is becoming an increasingly attractive destination for international investors, particularly amid global supply chain restructuring. It also provides domestic firms with access to capital, technology, and management expertise.

On the downside, the trend suggests that domestic enterprises are in a weaker position in terms of capital and financial capacity. Faced with rising costs and tightening cash flow, many are compelled to sell equity as a survival strategy.

More concerning is that if FDI continues to tilt heavily toward M&A without accompanying production expansion, the economy could experience capital growth without a corresponding increase in productive capacity. In such a scenario, FDI would no longer serve as a driver of new production capacity, but rather as a mechanism for reallocating ownership.

In the long term, a rising share of foreign ownership in domestic enterprises, especially in strategically-important sectors, could undermine economic independence and autonomy if not guided by appropriate screening and policy frameworks.

Moreover, compared with greenfield FDI, M&A flows tend to generate weaker technology spillovers, fewer supply chain links, and lower job creation, while posing higher risks of profit repatriation. In this context, attracting FDI is no longer just about scale or growth, but about quality, structure, and the extent of its real contribution to the economy. FDI policy must therefore shift from a focus on quantity to one on quality, ensuring that inflows expand productive capacity, increase value-added, and strengthen links with the domestic sector.

International trade surges & Competition recovers

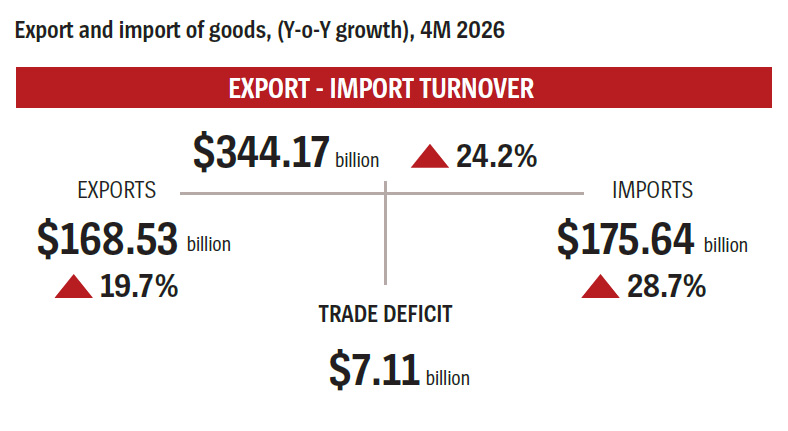

Total export and import turnover stood at $344.17 billion in the first four months, up 24.2 per cent. However, the trade balance shifted to a deficit of $7.11 billion; a notable reversal compared to the same period last year.

Monthly trade dynamics show imports growing faster than exports, reflecting enterprises’ efforts to ramp up raw material imports amid expectations of further price increases.

More notably, dependence on the FDI sector continues to deepen. Exports from this sector accounted for as much as 80 per cent of total export turnover, rising 25.8 per cent year-on-year, while exports from the domestic sector were nearly flat, increasing by just 0.4 per cent.

This underscores that export growth still relies heavily on the FDI sector, while the economy’s internal capacity has yet to improve proportionately. Though international trade is expanding strongly, its structure remains imbalanced, with growing dependence on FDI.

Total retail sales of goods and consumer service revenue increased by 6.3 per cent in the first four months, lower than the 7.7 per cent growth recorded in the same period of 2025 and below the 7 per cent growth seen in the first quarter.

Notably, this growth was partly supported by spending from 8.8 million international tourist arrivals to Vietnam, suggesting that domestic purchasing power and consumption demand are recovering only slowly.

Amid rising prices and eroding real incomes, consumers are tightening spending, weakening the role of domestic demand as a growth driver. The slow recovery of domestic demand is becoming a bottleneck for growth.

Stabilizing the macro-economy

Vietnam’s economy is currently facing a range of risks. Policy management therefore needs not only to support growth but also to focus on risk control, risk management, and restructuring the foundations and drivers of economic development.

First, priority should be given to controlling inflation and maintaining macro-economic stability. As cost-push inflation intensifies, monetary policy must be more flexible and prudent, avoiding excessive easing that could put further pressure on prices. Fiscal policy should be more proactive in reducing costs for businesses through targeted tax and fee deferrals, reductions, and exemptions.

Second, efforts should focus on reducing input costs across the economy, from logistics and energy to compliance costs. The government’s issuance of resolutions to cut administrative procedures is a timely and appropriate step, but effective implementation is critical to avoid a situation where procedures are “reduced on paper but unchanged in practice.”

Third, in the context of weak domestic demand, coordinated measures are needed to stimulate consumption in a sustainable manner, linked to improving real incomes and strengthening consumer confidence, rather than relying solely on short-term stimulus measures.

Fourth, FDI attraction policies should be reoriented toward improving quality. The goal should not only be to attract more capital but also to prioritize investment that creates new productive capacity, facilitates technology transfer, and strengthens links with domestic enterprises. Appropriate screening and monitoring mechanisms are needed for M&A transactions, particularly in key sectors.

Fifth, stronger development of the domestic business sector, especially industrial enterprises and those participating in value chains, is essential. Without enhancing internal capacity, the economy will remain dependent on the FDI sector, and structural risks will continue to increase.

Finally, improving the efficiency and spillover effects of public investment must become a top priority. Beyond accelerating disbursement, it is crucial to select projects that appeal to private investment and generate long-term growth momentum.

The first four months revealed that Vietnam’s economy has maintained its recovery momentum, with bright spots in production, investment, and international trade. However, inflationary pressures, rising costs, weak aggregate demand, and structural risks are posing significant challenges for macro-economic management.

As growth constraints become more apparent and increasingly interconnected, policy space is no longer as ample as before. This requires that macro-economic management be more proactive, flexible, and targeted, rather than broad-based.

In this context, maintaining macro-economic stability, controlling inflation, reducing costs, and strengthening the economy’s internal capacity will be decisive in securing growth quality going forward. At the same time, restructuring growth drivers toward a more balanced relationship between the domestic and FDI sectors, as well as between exports and domestic consumption, will be critical.

With the government’s commitment to reform, the National Assembly’s support, and the resilience of the business community, Vietnam’s economy has a solid basis to overcome its current constraints, successfully control inflation, strengthen internal capacity, and improve the quality of growth in the time ahead.

(*)Dr. Nguyen Bich Lam is the former Director General of the General Statistics Office, now the National Statistics Office, at the Ministry of Finance.

Google translate

Google translate