Vietnam’s business landscape in 2025 was marked by a surge in newly-registered enterprises and large capital inflows but the “shakeot” was equally remarkable, forcing companies to rethink their strategies in order to survive as others fall by the wayside.

According to data from the National Statistics Office (NSO) at the Ministry of Finance, nearly 17,200 new enterprises were set up nationwide in December alone, for a striking 71.6 per cent increase year-on-year. This not only reflects efforts to complete annual business plans but also signals strong investor expectations for a new growth cycle in 2026.

Encouraging indicators

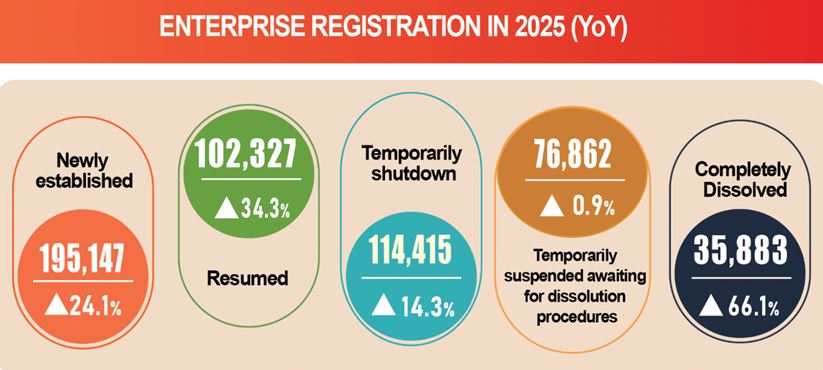

In 2025 as a whole, the total number of newly-registered enterprises reached 195,100, up 24.1 per cent against 2024. On average, around 16,300 new companies were created each month, injecting fresh energy into the labor market and production activities. Alongside this came a corresponding rise in registered capital, totaling VND1,919 trillion ($73.8 billion), and employment, with more than 1.15 million jobs added.

Notably, it was not only new enterprises that contributed to the vibrancy of Vietnam’s business landscape last year. The revival of many companies that temporarily suspended operations also played an important role, with 102,300 such companies resuming operations, up 34.3 per cent against 2024 and bringing their total number to 297,500. This record figure underscores the resilience and adaptability of Vietnam’s business community in the face of economic headwinds.

According to Ms. Phi Thi Huong Nga, Head of the Industry and Construction Statistics Department at the NSO, the return of temporarily inactive companies suggests that constraints related to capital, markets, and the legal framework have been at least partially eased, creating more favorable conditions for production to restart.

Another important aspect of last year’s business landscape is that the average registered capital of newly-registered enterprises remained at VND9.8 billion ($376,925), unchanged from 2024 despite the ongoing economic challenges. At this level, total additional registered capital injected into the economy stood at nearly VND6,400 trillion ($246.2 billion), up 77.8 per cent compared to 2024.

In particular, additional capital from existing enterprises exceeded VND4,400 trillion ($169.2 billion), surging 118.3 per cent. This points to strengthening internal capacity at Vietnamese businesses, as enterprises increasingly move beyond small-scale operations towards expansion and deeper investment.

By economic sector, 2025 saw a clear structural shift. The services sector continued to assert its role as a pillar of the economy, with 149,300 newly-registered enterprises, up 25.6 per cent. Wholesale and retail trade, transportation and warehousing, and accommodation and food services all recorded growth of more than 30 per cent in new registrations, driven by the recovery of tourism and domestic consumption.

Conversely, the construction sector exhibited worrying signs. It was one of just a few sectors to post a decline in newly-registered enterprises, of 0.5 per cent, while the rate of business dissolutions surged 83.3 per cent.

While the manufacturing and processing sector saw a sharp increase in dissolutions, of 68.5 per cent, it still maintained strong growth in new registrations, of 35.8 per cent. This suggests a sector characterized by intense competition and high attrition yet offering significant opportunities for firms with advanced technology and strong management capabilities.

Business exits

Alongside the bright spots in new business formation and reactivation, the high level of business exits in 2025 was another notable feature of the business landscape. On average, 18,900 enterprises exited the market each month. The number of companies temporarily suspending operations reached 114,400, up 14.3 per cent against 2024. Most strikingly, 35,900 enterprises completed dissolution procedures, a sharp increase of 66.1 per cent.

Explaining why record-high market entry coincided with a surge in dissolutions, the NSO pointed to the harsh selection mechanism inherent in a modern market economy. First, small and micro-sized enterprises often lack sufficient working capital and risk management capacity, making them vulnerable to even minor market fluctuations. Second, rising input costs, particularly labor and raw materials, have eroded profit margins for businesses operating under traditional models. Third, digital and green transitions are imposing new standards.

In addition, the growing number of enterprises ceasing operations while awaiting dissolution procedures, totaling 76,900, highlights persistent legal bottlenecks and debt burdens that remain difficult obstacles for inefficient businesses.

An analysis by the NSO of factors affecting production and business activities in the fourth quarter of 2025 also points to several key challenges. Though interest rates have stabilized, access to low-cost capital remains problematic for small and medium-sized enterprises (SMEs). Moreover, while the number of service enterprises has increased, consumers remain circumspect when it comes to purchases, leading to inventory build-ups in certain sectors.

Optimistic outlook

Despite these challenges, surveys on business trends in the fourth quarter show that enterprises remain cautiously optimistic about their near-term prospects. Some 75.8 per cent of respondents expect their business performance to improve or remain stable compared with the previous quarter; an important sign that market sentiment is gradually stabilizing.

By ownership type, State-owned enterprises and foreign-invested enterprises (FIEs) displayed stronger optimism. Their balance indices - the percentage of respondents reporting improvement minus those reporting deterioration - stood at 5.5 per cent and 5.3 per cent, respectively, positioning these sectors as economic anchors.

The stability of the FDI sector indicates that Vietnam continues to be an attractive destination within global supply chains, despite the geopolitical uncertainties. By contrast, non-State enterprises, while accounting for the majority of firms, recorded a balance index of just 0.2 per cent, reflecting ongoing competitive pressures and financial risks facing the private sector.

By sector, manufacturing and processing emerged as the most optimistic, with a balance index of 14.3 per cent, driven by a recovery in export orders towards year’s-end and stronger consumption during the holiday season. Conversely, trade and services, despite high rates of new business registrations, posted a negative balance index of -2.5 per cent. This serves as a warning about weak purchasing power in certain segments and mounting pressure from cross-border e-commerce on traditional retail models.

Assessing the overall business landscape in 2025, the NSO noted that although nearly 300,000 enterprises entered or re-entered the market, the sharp rise in dissolutions underscores the need for more effective support measures to foster sustainable business development in 2026. These include credit guarantee mechanisms for SMEs, administrative reforms, particularly in dissolution and suspension procedures, and stronger promotion of digital transformation in services and retail to boost productivity and competitiveness.

Google translate

Google translate