Vietnam’s economy is standing at a historic turning point, marking a transition from a development model based on labor and capital intensity to one driven by productivity, innovation, and efficient resource allocation. The five-year socio-economic development plan for 2026-2030, unanimously approved by the National Assembly, sets out highly-ambitious macro-economic goals: positioning Vietnam among the world’s Top 30 economies by GDP size, achieving per capita income of $8,500 by 2030, and maintaining average annual GDP growth of 10 per cent or higher.

New growth era

During the reform period, the policies and perceptions of the Party and the State regarding the private sector and FDI have undergone a profound transformation, from cautious restriction to proactive encouragement, recognizing them as key drivers of the socialist-oriented market economy. This evolution can be divided into five milestone phases.

First, 1986-1996 (6th and 7th Party Congresses - Initiation of Reform): The Party began acknowledging a multi-sector economy, allowing the private sector to operate under State management. The promulgation of the Law on Foreign Investment in Vietnam in 1987 laid the first legal foundation for attracting international capital and opening the economy.

Second, 1996-2006 (8th, 9th, and 10th Party Congresses - Role Affirmation): The 9th Congress in 2001 marked a major shift in thinking, by officially recognizing the private sector as an equal and long-term component of the economy. The 10th Congress in 2006 further broke new ground by permitting Party members to engage in private business. The FDI environment became more open, alongside efforts to refine market economy institutions.

Third, 2006-2016 (11th and 12th Party Congresses - Key Driver): The private sector was officially affirmed as an “important driver.” Policies focused on fostering large-scale private economic groups. FDI flows were increasingly directed toward high-tech and environmentally-friendly sectors.

Fourth, 2016-2026 (12th and 13th Party Congresses - Most Important Driver): A major turning point came with Resolution No. 10-NQ/TW in 2017, shifting FDI attraction toward a “selective, high-quality” approach, prioritizing advanced technologies, modern governance, and strong spillover effects. Crucially, it emphasizes tighter links with domestic enterprises. The private sector now contributes approximately 55-58 per cent of GDP and generates over 84 per cent of employment, while FDI has become a core pillar of export capacity and structural transformation.

Fifth, 2026-2030 (14th Party Congress - Second Reform Era): Defined as a new wave of reform, Politburo Resolution No. 68-NQ/TW, signed on May 4, 2025, identifies the private sector as the most important driver, playing a pioneering role in innovation and digital transformation.

The development trajectory in this unprecedented era demands a comprehensive structural transformation across all dimensions of the investment ecosystem. To realize breakthrough ambitions, Vietnam must resolve the challenge of mobilizing enormous financial resources. Total social investment demand for 2026-2030 is estimated at a minimum of VND38,500 trillion ($1.5 trillion), or approximately 40 per cent of GDP.

Meanwhile, the State budget is expected to allocate VND8,220 trillion ($316 billion) for medium-term public investment, covering only 21-22 per cent of total demand. Nearly 80 per cent of the remaining financial burden must therefore be mobilized from the domestic private sector and FDI.

As the traditional banking credit system reveals limitations in medium and long-term lending capacity, unlocking the full productive potential of the economy requires a well-developed, transparent investment ecosystem, lubricated by efficient capital markets and breakthrough legal frameworks.

Investment ecosystem challenges

A trade deficit of $7.11 billion in early 2026 has raised alarms about structural weaknesses in the domestic sector and dependence on imported inputs, while also reflecting a cycle of capital accumulation for production expansion. To address the imbalance between domestic private enterprises and foreign-invested sectors, and to achieve the 10 per cent GDP growth target, the economy must rely on a synchronized growth engine rather than export processing driven solely by FDI.

This includes a “revolution” in disbursing VND8,220 trillion ($316 billion) in public investment to create strategic infrastructure “seed capital” and reduce the Incremental Capital-Output Ratio (ICOR) to 3.5. It also involves reorganizing economic space into five key growth regions and next-generation free trade zones. Policy reforms, exemplified by Politburo Resolution No. 68, aim to remove legal barriers, allocate land, and implement controlled sandbox mechanisms to nurture 2 million tech-enabled private enterprises.

At the same time, FDI inflows of $18 billion must be reoriented toward core sectors such as semiconductors, AI, and green energy, with mandatory deep links to domestic supply chains through circular and symbiotic economic models.

The planned upgrade of the stock market this September will act as a “financial valve,” channeling long-term international capital, easing pressure on the banking system, and fueling domestic enterprises’ global competitiveness. The convergence of these frameworks and financial solutions will reshape the national economic structure and propel Vietnam into a new era of prosperity.

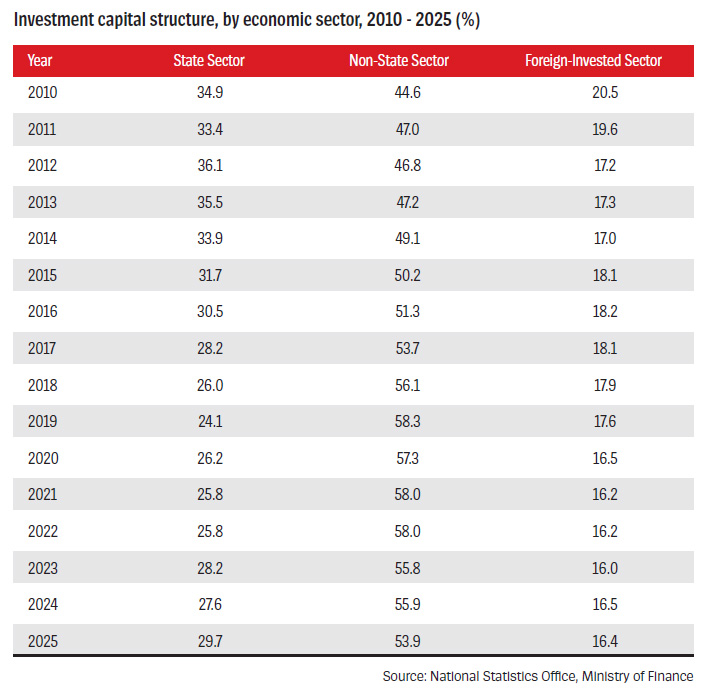

Growth momentum is increasingly driven by the rise of the domestic private sector. Its contribution to GDP increased from 44.6 per cent in 2010 to 58.3 per cent in 2019 and has remained stable at around 56-58 per cent in the post-pandemic recovery years. Meanwhile, the State sector’s share declined from nearly 35 per cent to around 26-27 per cent, reflecting ongoing equitization, divestment, and reduced direct State intervention in production and business activities.

Though FDI accounts for only 16-20 per cent of total social investment, it dominates export capacity and high-tech supply chains. The rising share of private capital highlights the dynamism and capital accumulation capacity of domestic enterprises. However, this vast capital has not translated proportionally into core competitiveness. Vietnam’s private sector remains dominated by micro, small, and medium-sized enterprises (MSMEs), and lacks leading firms capable of driving supply chains. Despite contributing nearly 60 per cent of investment capital, the domestic private sector remains weak in international trade.

Investment in mining has declined sharply, from VND62.7 trillion ($2.4 billion) in 2010 to VND17.2 trillion ($660 million) in 2024, consistent with a strategic shift away from raw resource exports toward higher value-added products. Meanwhile, investment in manufacturing has steadily increased, reaching VND563.4 trillion ($21.7 billion) in 2024 and maintaining its position as the most attractive sector. However, most of the surplus value and high-tech content in manufacturing remains under FDI control, exposing vulnerabilities in the domestic production sector amid global economic cycles.

The fragility of the domestic private sector is further revealed by the reversal of the trade balance in the first four months of 2026. Vietnam posted a trade deficit of $7.11 billion, compared to a surplus of $4.3 billion in the same period of 2025. The contrast is stark: the FDI sector accounts for 80 per cent of total exports and maintains a trade surplus of $8.5 billion, while the domestic sector exports only $33.65 billion, with negligible growth of 0.4 per cent, but imports heavily, resulting in a massive deficit of $15.61 billion. Consequently, the FDI surplus can no longer offset the domestic deficit, pushing the entire economy into a trade imbalance.

On the positive side, this signals the early stage of a production expansion cycle. Notably, 94.2 per cent of total imports, worth $165.37 billion, consist of production inputs, including machinery (54.8 per cent) and raw materials (39.4 per cent). However, the risks are significant: heavy dependence on imported inputs exposes a critical vulnerability in the investment ecosystem.

Geopolitical disruptions, such as tensions in the Middle East affecting logistics and energy price volatility, could immediately erode profit margins for domestic enterprises. Unlocking resources to achieve partial self-reliance in raw material supply chains has therefore become an urgent priority in national investment policy.

Public investment as “seed capital”

To establish a robust infrastructure foundation capable of absorbing VND30,000 trillion ($1.15 trillion) from the private sector and foreign investment, including both FDI and portfolio investment, the government has launched a “revolution” in the 2026-2030 Medium-Term Public Investment Plan, with a total scale of VND8,220 trillion ($316 billion). Of this, the central budget accounts for VND3,800 trillion ($146 billion) and local budgets VND4,420 trillion ($170 billion).

The core challenge in achieving the 10 per cent annual growth target while maintaining an investment-to-GDP ratio of 35-40 per cent lies in improving capital efficiency, reducing the ICOR from 6.4 in the 2021-2025 period to 3.5-4.0 in 2026-2030. Vietnam’s historically-high ICOR largely stems from inefficiencies in State-owned enterprises, stagnation in the real estate sector, and prolonged heavy industrial projects. Directive No. 16/CT-TTg, issued on April 23, 2026 by the Prime Minister, establishes strict discipline over public capital flows, requiring that projects meet Economic Internal Rate of Return (EIRR) criteria based on socio-economic accounting and demonstrate both direct and indirect spillover value.

Approximately 30 per cent of the project pipeline has been cut to prevent fragmented and scattered investment. Around 75 per cent of central budget capital is concentrated on national target programs and strategically-important inter-regional projects. A breakthrough in land clearance policy allows site clearance to be separated into independent projects and implemented prior to main project approval, eliminating cost overruns and legal disputes.

Decentralization is strengthened through “block grant” capital allocation to localities under the principle of “localities decide, localities implement, localities take responsibility.” The State commits to providing a secure legal framework to protect proactive officials, removing risk-averse attitudes that have hindered administrative efficiency. At the same time, efforts are focused on resolving legal bottlenecks for over 3,000 “frozen” real estate projects, which could contribute 5-7 per cent to GDP and directly reduce the economy-wide ICOR.

Infrastructure as a catalyst

Public capital reallocation is materialized through mega-projects reshaping economic connectivity. The National Assembly has approved over VND192 trillion ($7.4 billion) in central budget funds to continue and initiate nationally significant projects. By 2030, Vietnam aims to complete at least 5,000 km of expressways, connecting key arteries such as the Eastern North-South Expressway, East-West corridors (Chau Doc - Can Tho - Soc Trang, Bien Hoa - Vung Tau, and Khanh Hoa - Buon Ma Thuot), and ring roads around Hanoi and Ho Chi Minh City.

Priority is also given to the North-South high-speed railway and the Lao Cai - Hanoi - Hai Phong international rail corridor, alongside urban rail systems in Hanoi and Ho Chi Minh City. This synchronized infrastructure network acts as “seed capital,” reducing logistics costs from the current 20 per cent of GDP to 13-15 per cent, thereby directly increasing profit margins for private and FDI enterprises.

The updated National Master Plan (2021-2030, with a Vision to 2050) outlines a fundamentally new economic map following administrative consolidation from 63 cities and provinces to 34 provincial-level units. This restructuring creates economic entities of sufficient scale for capital accumulation, optimizes urban planning, eliminates fragmentation, and concentrates resources into five key national growth regions: the Northern Growth Pole (centered on Hanoi), the Southern Growth Pole (centered on Ho Chi Minh City), the North Central Region, the Central Region (centered on Da Nang), and the Mekong Delta Region.

Cross-border economic corridors such as Lao Cai - Hanoi - Hai Phong - Quang Ninh and Moc Bai - Ho Chi Minh City - Bien Hoa - Vung Tau are defined as backbone axes for capital flows.

Next-generation free trade zones mark an institutional breakthrough, allowing foreign investors to establish economic entities without requiring prior investment project approval and exempting initial investment registration certification. These zones aim to integrate seaport logistics, international financial services, and high technology into closed-loop ecosystems.

Politburo Resolution No. 68 establishes the highest-level legal and ideological foundation for private sector development, officially identifying it as the “most important driver” and “pioneering force” of the economy. The Resolution introduces structural policy interventions targeting key constraints faced by private enterprises.

To address industrial land shortages - a critical bottleneck - localities are required to allocate at least 20 ha per industrial park or reserve 5 per cent of industrial land funds for high-tech firms, MSMEs, and innovative startups. A subsidy package reducing land rental costs by at least 30 per cent during the first five years lowers fixed costs, enabling private capital to focus on R&D and production upgrades.

The Resolution also introduces regulatory sandbox frameworks for AI, blockchain, and fintech business models, helping Vietnam keep pace with global innovation and attract venture capital into the domestic tech ecosystem. The State commits to ending delayed payments by public entities to private firms and strengthening contract enforcement to build investor confidence.

Targets include reaching 2 million active enterprises by 2030 (contributing 55-58 per cent of GDP) and developing at least 20 large private conglomerates capable of leading global supply chains. This is supported through public procurement preferences and training 10,000 globally-qualified CEOs, aiming to reverse the persistent trade deficit in production inputs.

Vietnamese private capital is increasingly expanding abroad. As of the end of 2024, outward FDI reached 1,825 projects with total registered capital of $22.64 billion, focusing on strategic markets such as Laos ($5.71 billion), Cambodia ($2.93 billion), and Russia ($1.62 billion). Investment sectors include mining ($7.03 billion), agriculture ($3.39 billion), and manufacturing ($1.77 billion), reflecting efforts by Vietnamese conglomerates to secure resources and markets for global supply chain integration.

Meanwhile, inbound FDI is entering a phase of qualitative refinement. In the first four months of 2026, total registered FDI stood at $18.24 billion, up 32 per cent year-on-year, with disbursed capital estimated at $7.4 billion; the highest in five years. Manufacturing continues to dominate, attracting $10.49 billion, or 68.6 per cent of total newly-registered and additional capital.

Mobilizing investment capital

Vietnam’s FDI strategy has shifted from quantity to quality, focusing on building domestic-foreign links and global integration. As multinational corporations restructure supply chains, competitiveness is no longer based on low labor costs but on adaptability, transparency, and sustainability of local industrial ecosystems.

However, localization rates remain low, with Vietnamese firms primarily engaged in low-value assembly, resulting in large trade deficits in production inputs. The key to transformation lies in domestic private enterprises, especially support industries, proactively upgrading technology and environmental, social, and governance (ESG) standards to become Tier-1 suppliers for FDI firms. Successful domestic firms demonstrate that flexibility in meeting FDI partners’ requirements - quality, delivery time, integrated logistics services - is critical to gaining trust and gradually mastering supply chains.

Collaboration with high-tech corporations willing to share value and transfer technology is essential. Ecosystem-based investment models, particularly those applying circular economy principles and Gunter Pauli’s blue economy “cascade” model, can deepen links between domestic private firms and FDI. In this model, waste or by-products from one industry become valuable inputs for another, eliminating the concept of waste and creating closed-loop value chains with economic, environmental, and social benefits.

In Vietnam, eco-industrial parks will serve as hubs where leading FDI firms and domestic satellite enterprises form industrial symbiosis networks, sharing resources, surplus energy, treated wastewater, and recycled materials. This reduces operational costs, conserves resources, meets stringent ESG standards, and enables “Made in Vietnam” products to overcome carbon tariffs while contributing directly to the country’s net-zero emissions by 2050 goal.

To mobilize 80 per cent of the VND38,500 trillion ($1.5 trillion) in total investment required for the 2026-2030 period, the capital market, particularly the stock market and corporate bond market, must take on a historic role. The traditional banking system has reached its limits in using short-term capital for medium and long-term lending, posing systemic liquidity risks.

In April, FTSE Russell confirmed that Vietnam had removed key technical barriers in its stock market, including pre-funding requirements and the adoption of a Global Broker model, and is now officially on track for an upgrade from “Frontier Market” to “Secondary Emerging Market.” This upgrade is expected to trigger inflows of $1.5-1.67 billion from index-tracking funds such as Vanguard into approximately 30 leading Vietnamese stocks. The broader spillover effect, combined with transparency reforms, could attract between $10-25 billion in international capital over the long term.

With Emerging Market status, Vietnam’s market P/E ratio is expected to increase by 1-2 points, narrowing the valuation gap with regional peers and boosting market capitalization. This creates favorable conditions for domestic firms to raise international capital through equity and bond issuance at significantly lower costs, supporting merger and acquisition (M&A) and high-tech R&D investments.

Market liquidity is projected to stabilize at $1.3-2.1 billion per session. Pressure from high-standard foreign capital will require Vietnamese listed companies to enhance transparency, adopt international accounting standards (IFRS), improve corporate governance, and implement ESG practices, thereby protecting investors and filtering out unsustainable businesses.

New mechanisms, such as allowing State-owned commercial banks to increase charter capital from retained earnings, providing tax incentives for investment funds, and permitting FDI enterprises to list on domestic exchanges, will create a powerful endogenous capital circulation cycle.

Google translate

Google translate