The sovereign credit rating development observed in Vietnam during January represents a rare structural inflection within global sovereign finance, reflecting a precise interaction between legacy debt architecture and contemporary rating methodology rather than a cyclical improvement driven by macro-economic momentum alone.

Structural upgrade

On January 22, Fitch Ratings upgraded Vietnam’s senior secured long-term foreign currency debt instruments, specifically the Brady Bonds issued during the 1998 London Club restructuring, from BB+ to BBB-, marking the first instance in which a Vietnamese sovereign-linked instrument attained an explicit investment-grade classification.

The upgrade applied exclusively to secured instruments rather than the sovereign issuer itself, whose long-term foreign currency Issuer Default Rating remained anchored at BB+, thereby establishing a formal differentiation between probability of default and loss severity within the Vietnamese credit complex.

This distinction emerged following Fitch’s September 2025 revision of sovereign rating criteria, which introduced granular recovery assumptions into sovereign analysis and enabled legally-protected collateral structures to generate rating outcomes independent from the unsecured sovereign ceiling. Through this methodological evolution, Fitch recognized that the US Treasury zero-coupon bonds securing the principal of Vietnam’s Brady instruments materially altered expected recovery outcomes under stress scenarios, producing loss characteristics inconsistent with speculative-grade classification even under adverse sovereign credit events.

The rating divergence highlights a deeper structural narrative concerning Vietnam’s integration into global capital markets and the enduring consequences of late 20th-century debt resolution strategies.

The Brady Bonds originated as instruments of reintegration following decades of economic isolation, default, and post-war reconstruction, carrying design features that embedded external credibility into Vietnam’s external obligations during a period when institutional capacity remained limited. Full principal collateralization through offshore-held US Treasury securities, supplemented by rolling interest guarantees funded through high-grade assets, transformed these instruments into quasi risk-insulated claims whose performance depended less on sovereign discretion than on contractual enforcement mechanisms beyond domestic jurisdiction.

Fitch’s recovery analysis quantified this insulation by assigning superior recovery expectations that justified a one-notch uplift beyond the sovereign anchor, though methodological constraints capped further elevation due to residual exposure linked to coupon interruption risk, legal execution friction, and sovereign-linked payment continuity. The resulting BBB- classification therefore reflects neither optimism regarding issuer strength nor market sentiment regarding Vietnam’s political trajectory, instead representing a mathematically-derived assessment of recovery certainty embedded in instrument design.

While the secured debt upgrade attracted attention for breaching the investment-grade threshold, the sovereign rating environment in 2026 will continue to reflect unresolved structural constraints that extend beyond macro-economic performance indicators.

Vietnam’s economic expansion remained among the strongest within the Asia-Pacific region, supported by sustained FDI inflows, industrial diversification, export resilience, and expanding participation in semiconductor value chains. Public debt ratios remained contained well below statutory limits, foreign exchange reserves recovered towards historical highs, and external balances maintained surplus positions that buffered exchange rate volatility. These quantitative strengths aligned favorably against peers already holding investment-grade sovereign ratings, reinforcing the perception of Vietnam as a high-performing outlier within speculative-grade classifications. The absence of a sovereign upgrade therefore did not arise from fiscal imbalance or external vulnerability, instead originating from qualitative institutional assessments that remain central to sovereign rating frameworks.

Governance metrics continue to represent the dominant constraint within Vietnam’s sovereign credit profile, exerting downwards pressure through institutional transparency, regulatory predictability, and legal consistency assessments embedded within rating agency methodologies. Vietnam’s positioning within the lower half of global governance percentile rankings reflects persistent concerns regarding administrative discretion, data disclosure timeliness, enforcement clarity, and procedural predictability for creditors. These characteristics elevate policy execution risk despite stable macro-economic management, limiting confidence regarding dispute resolution, capital mobility assurances, and crisis coordination capacity under stress conditions.

The ongoing anti-corruption campaign reinforced this tension by improving long-term structural integrity while simultaneously constraining short-term administrative throughput, generating approval delays and decision bottlenecks across public investment and regulatory channels. Rating agencies interpreted this environment as stable yet constrained, maintaining outlook stability while refraining from upwards revision absent demonstrable institutional consolidation.

The secured debt upgrade therefore carries strategic implications that extend beyond the maturing Brady instruments themselves, serving as an empirical demonstration of how structural credit enhancement can partially substitute for institutional weakness within sovereign financing frameworks. The successful recognition of recovery-driven rating uplift establishes a precedent for Vietnam’s future engagement with structured finance mechanisms, particularly within infrastructure development, climate transition financing, and multilateral-supported issuance formats. Partial guarantees, escrow-based revenue securitization, and multilateral risk-sharing arrangements offer pathways for accessing investment-grade funding channels prior to full sovereign upgrade attainment, enabling capital mobilization aligned with development priorities.

These mechanisms complement rather than replace the longer-term objective of sovereign rating elevation, which remains contingent upon governance modernization, financial sector fortification, and regulatory transparency advancement.

The January rating action therefore occupies a dual symbolic role within Vietnam’s sovereign narrative, representing validation of historical debt architecture while simultaneously underscoring the remaining distance separating secured instrument excellence from issuer-wide investment-grade status.

The Brady Bonds demonstrate that recovery certainty can be engineered even within constrained institutional environments, though such certainty remains externalized rather than internally generated. The sovereign rating anchor continues to reflect the State’s institutional maturity rather than its economic vitality, reinforcing the conclusion that governance reform represents the decisive variable within Vietnam’s credit trajectory towards 2030.

Until institutional reliability converges with macro-economic strength, Vietnam’s sovereign profile will continue to exhibit bifurcation between structurally-protected obligations and unsecured sovereign exposure, positioning the country as a near investment-grade credit defined less by economic insufficiency than by institutional evolution lag.

2026 bond market

Vietnam’s bond market entering 2026 reflects a phase of structural transformation shaped by post-crisis discipline, regulatory consolidation, and strategic redirection towards sustainable capital allocation.

After the liquidity shock experienced during 2022 and 2023, market participants underwent a prolonged adjustment period marked by balance sheet repair, investor confidence rebuilding, and institutional learning. As of early 2026, outstanding corporate bonds had reached approximately VND1,400 trillion ($53.71 billion), equivalent to nearly 11 per cent of GDP and indicating a recovery of scale accompanied by notable qualitative shifts.

Issuers increasingly operate under stricter disclosure standards, investor scrutiny has intensified, and pricing differentiation based on credit quality has become visible across tenors and sectors. Banking institutions dominate issuance activity due to capital buffer requirements under Basel II and Basel III frameworks, while property developers access the market primarily for refinancing purposes rather than expansion. The resulting structure reveals a segmented market where capital efficiency and credit transparency determine access conditions, signaling a transition away from speculative issuance patterns towards a rules-based, fixed-income environment.

Macro-economic policy orientation will play a decisive role in shaping bond market dynamics during 2026, particularly through ambitious growth objectives and calibrated monetary management. Government planning documents emphasize accelerated economic expansion supported by infrastructure investment, industrial upgrading, and energy transition financing, generating funding needs beyond traditional bank credit capacity.

Monetary authorities maintain a credit growth target near 15 per cent, accompanied by qualitative guidance prioritizing production, business activity, and environmentally-aligned sectors. Such guidance reshapes capital flows by channeling bank liquidity towards manufacturing and green projects while compelling real estate enterprises to rely on bond financing under higher yield expectations.

Interest rate conditions stabilized after short-term liquidity pressure observed at the end of 2025, with deposit benchmarks anchoring corporate bond pricing within a range compatible with medium-term investment planning. Exchange rate stability further reinforces market attractiveness, as the VND demonstrates resilience against external volatility, reducing currency risk premiums for foreign investors evaluating sovereign and corporate fixed-income exposure.

Sovereign debt developments during early 2026 add an additional structural layer to the bond market landscape through differentiated credit assessment rather than broad-based rating revision. The upgrade of senior secured external debt instruments to investment-grade status reflects the application of recovery-based rating methodology recognizing offshore collateral structures embedded within legacy obligations.

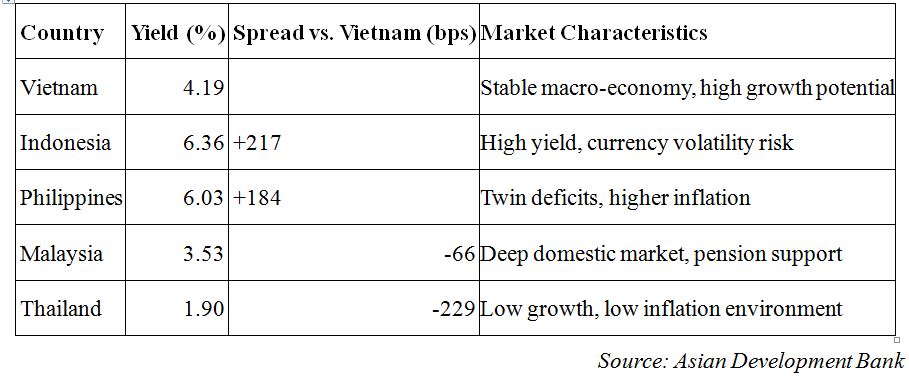

Such recognition establishes a precedent for credit enhancement effectiveness without altering the unsecured sovereign rating, which remains constrained by governance metrics and institutional capacity assessments. Government bond yields respond primarily to supply conditions linked to public investment disbursement and refinancing needs, producing a yield curve that balances growth expectations with liquidity competition from private sector borrowing. Relative to regional peers, Vietnam occupies an intermediate yield position that combines currency stability with growth-linked return potential, reinforcing demand from regional funds seeking diversification without excessive volatility exposure.

Regulatory architecture and sustainable finance initiatives will define the forward-looking dimension of the bond market during 2026 through enforcement discipline and thematic capital mobilization. The reinstatement of stringent issuance conditions following the expiration of temporary relief measures reshapes the investor base towards institutions capable of absorbing disclosure complexity and credit assessment requirements. Mandatory credit ratings reduce information asymmetry while discouraging issuance lacking structural support or repayment visibility.

Parallel to regulatory tightening, the introduction of a national green classification framework establishes formal eligibility standards for environmentally-aligned projects, enabling sovereign and corporate issuers to access thematic capital pools linked to climate objectives. Planned pilot issuance of green government bonds creates a reference curve supporting pricing discovery for sustainable corporate instruments, aligning domestic capital markets with international environmental finance flows. Through these combined mechanisms, Vietnam’s bond market in 2026 will evolve into a platform where regulatory credibility, credit differentiation, and sustainability alignment collectively determine capital access, reinforcing resilience while supporting long-term development objectives.

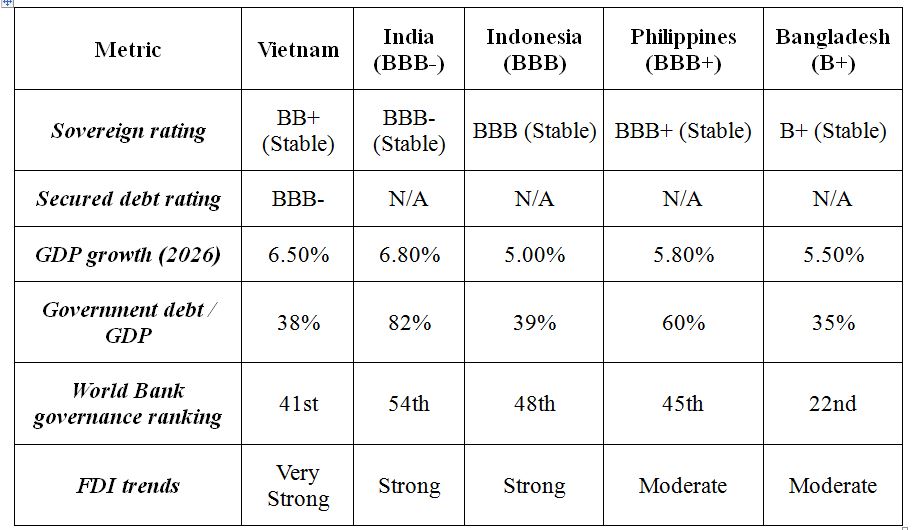

Credit ratings - Vietnam & other Asian countries

Comparison of Vietnam’s sovereign yields with regional peers

Google translate

Google translate