Vietnam’s economy maintained its solid recovery trajectory over the course of the first five months of 2026, with bright spots found in industrial production, public investment, FDI inflows, and international goods trade. Behind the growth figures, however, several emerging concerns warrant close attention: mounting inflationary pressure, a widening trade deficit, sluggish domestic demand, and a growing dependence on the FDI sector. These developments suggest that the economy is entering a phase in which the challenge is no longer simply to grow faster but to become more self-reliant and achieve more sustainable growth.

Industrial production

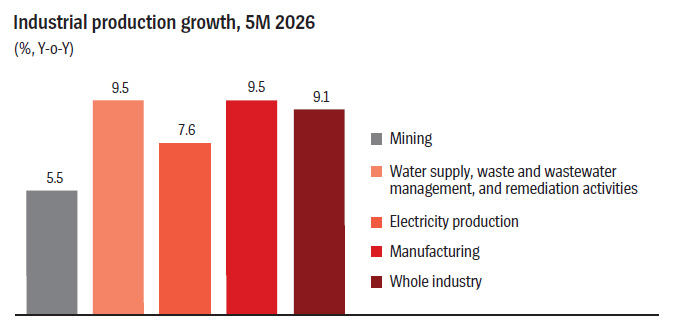

The Index of Industrial Production (IIP) rose 9.1 per cent year-on-year in the first five months, 0.3 percentage points higher than the growth recorded during the same period of 2025. It also marked the strongest five-month performance in four years.

The manufacturing and processing sector remained the primary growth driver, making the largest contribution to industrial output, exports, and job creation. The result underscores the resilience and adaptability of Vietnam’s manufacturing base despite continued uncertainty in the global economy.

The expansion in industrial production also reflects the initial effectiveness of policies aimed at supporting businesses, accelerating public investment, and improving the business environment.

Industrial production continues to be a key pillar of economic growth. However, the quality of the recovery is facing increasing pressure from rising input costs and external volatility.

Still, industrial output data only captures the sector’s end-results. To assess the quality and sustainability of the recovery, it is necessary to examine leading indicators such as new orders, production volumes, and business sentiment. These trends were reflected clearly in the Manufacturing Purchasing Managers’ Index (PMI) for May, which rose to 52.8 points from 50.5 points in April.

Output expanded for the 13th consecutive month, with growth accelerating significantly from March and April. New export orders returned to growth after two months of decline. Purchasing activity and inventories of raw materials also increased substantially. Yet these positive signs should be interpreted with caution.

The rise in orders and purchasing activity during May did not stem entirely from stronger aggregate demand. Rather, much of the increase reflected businesses’ efforts to hedge against potential supply chain disruptions linked to the conflict in the Middle East. Many companies proactively increased inventories of raw materials and goods to protect themselves against future price shocks and supply shortages. As a result, current growth signs appear to be driven more by risk mitigation than by genuine market demand.

More importantly, input costs increased for the fourth consecutive month, hitting the fastest pace of growth since April 2011. Rising prices for imported materials, fuels, and logistics services forced many manufacturers to raise their selling prices. This not only affects profitability and competitiveness but also increases inflationary pressure across the broader economy.

The rebound in the PMI reflects a recovery in manufacturing activity, but much of the momentum appears to be driven by precautionary behavior rather than a durable improvement in demand. The PMI data suggests, however, that manufacturing remains on a growth path despite mounting cost pressures.

However, economic health is measured not only by production activity but also by the ability of businesses to enter, survive, and expand. Against that backdrop, business formation and market exits during the first five months provide additional insights.

Business formation rises sharply

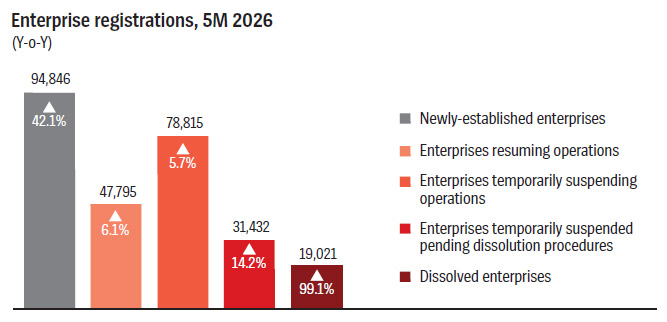

Vietnam recorded 94,800 newly-established enterprises in the five-month period, up 42.1 per cent year-on-year. Combined with nearly 47,800 businesses resuming operations after a period of temporary suspension, total market entrants reached 142,600 enterprises.

This is a positive sign, indicating a significant improvement in business confidence compared with last year. However, 74.47 per cent of newly-established enterprises were concentrated in the services sector, while growth in new industrial and manufacturing enterprises remained modest. On average, each newly-established enterprises registered only 4.5 employees and average charter capital of VND11.2 billion ($431,000).

These figures suggest that while the number of new businesses is rising rapidly, their scale remains small and their contribution to new productive capacity is limited. Most new enterprises continue to focus on trade and services rather than expanding the economy’s manufacturing base.

At the same time, 78,800 businesses suspended operations, more than 31,400 ceased operations pending dissolution, and over 19,000 completed dissolution procedures. In total, 129,200 enterprises exited the market, equivalent to 90.6 per cent of the number entering the market. This ratio indicates that the business environment remains challenging, particularly for small and medium-sized enterprises (SMEs).

More businesses are entering the market, but resilience and business quality remain unresolved challenges. For an economy as open as Vietnam’s, corporate performance is closely tied to international market conditions. Therefore, in addition to domestic business indicators, trade data remains a critical gauge of competitiveness and economic resilience.

Trade deficit widens

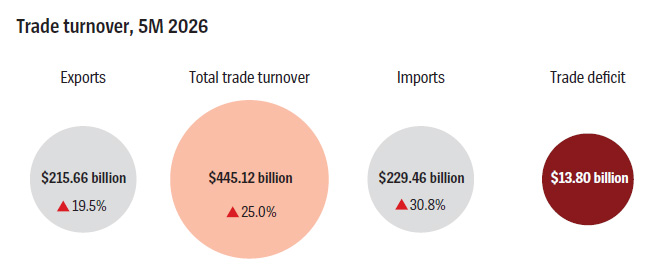

Vietnam’s total goods trade turnover stood at $445.12 billion in the first five months of 2026, up 25 per cent year-on-year. Exports totaled $215.66 billion, increasing 19.5 per cent, while imports surged 30.8 per cent to $229.46 billion, resulting in a trade deficit of $13.8 billion.

Notably, the trade deficit in May reached $5.21 billion, exceeding the $3.99 billion deficit recorded in April.

The trend suggests that many businesses have accelerated imports of materials and goods as a precaution against supply chain disruptions and price volatility associated with the conflict in the Middle East.

While higher imports may help businesses manage risks and maintain production, they also highlight the manufacturing sector’s heavy reliance on imported inputs.

Another notable feature is the continued dominance of the FDI sector in exports. Of the $215.66 billion in total exports, FDI enterprises accounted for $172.16 billion, up 24.7 per cent and representing 79.8 per cent of the total. The domestic sector generated only $43.5 billion in exports, up 2.5 per cent and accounting for just 20.2 per cent.

The widening gap underscores the limited participation of Vietnamese enterprises in global value chains. While exports are growing rapidly, the economy’s domestic export capacity is not keeping pace with the expansion of the FDI sector.

FDI inflows

FDI attraction remained another bright spot during the first five months of 2026. Yet behind the impressive growth figures lies a larger question: Is Vietnam strengthening its internal economic capacity, or becoming relatively weaker?

During the period, 1,576 new FDI projects were licensed with total registered capital of $14.84 billion; more than double the level recorded a year earlier. Disbursed FDI reached $9.75 billion, up 9.6 per cent for the highest five-month growth rate in five years.

However, the composition of FDI inflows deserves close monitoring. Of total registered FDI, $4.19 billion came from capital contributions and share acquisitions, up 46.7 per cent year-on-year. In May alone, such transactions totaled $1.68 billion, accounting for more than 40 per cent of the five-month total.

Most notably, foreign investors completed 828 acquisitions of stakes in domestic companies without increasing charter capital, with a combined value of $3.62 billion. This means that a substantial portion of FDI inflows is not directly creating new production capacity or jobs. Rather, ownership of existing domestic assets is being transferred from local investors to foreign investors.

From a market perspective, such transactions are a normal feature of an open economy. From a long-term development perspective, however, they raise two concerns. First, many domestic enterprises may be struggling with capital shortages, technology gaps, and competitive pressures, prompting them to sell equity stakes to foreign partners. Second, if the trend persists, Vietnam risks becoming increasingly dependent on the FDI sector, potentially weakening its economic autonomy. The issue is not the amount of FDI entering the country, but rather the growing share of investment directed toward acquiring existing assets instead of creating new productive capacity.

Domestic consumption

Retail sales of goods and consumer service revenues increased just 6.1 per cent during the first five months of 2026, below the 7.2 per cent growth rate recorded during the same period last year and slower than growth recorded in the first four months of the year. This occurred despite Vietnam welcoming 10.6 million international visitors, up 14.9 per cent and the highest level ever recorded. Without the boost from international tourism, underlying household demand would appear even weaker.

The data suggests that household incomes have not improved sufficiently to offset rising consumer prices. Inflationary pressures continue to encourage cautious spending behavior among consumers. The economy is unlikely to achieve sustainable growth if household consumption recovers more slowly than production and investment.

Weak consumer demand reflects not only modest income growth but also the increasingly visible impact of rising prices. With business input costs continuing to rise and global energy prices remaining elevated, inflation has become one of the most pressing macro-economic concerns.

Rising inflation

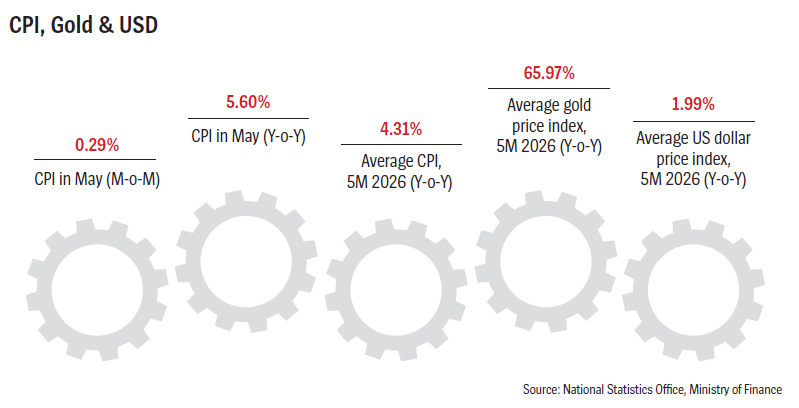

The Consumer Price Index (CPI) increased 5.6 per cent year-on-year in May and 4.31 per cent during the first five months, while core inflation rose 4.04 per cent. These figures are relatively high given the dual objective of maintaining macro-economic stability while pursuing double-digit economic growth.

Current inflation is largely cost-push in nature. Higher raw material prices, rising logistics costs, exchange rate pressures, and elevated global energy prices are all contributing factors.

Under the World Bank’s baseline scenario, assuming the most severe disruptions ease and shipping through the Strait of Hormuz gradually returns to near pre-conflict levels by the end of the year, Brent crude oil prices are projected to average $86 a barrel in 2026, up 24.6 per cent from $69 per barrel in 2025. This factor alone could add approximately 1.1 percentage points to the CPI.

At the same time, expanded public investment and adjustments to State-administered prices for selected goods and services could place additional upward pressure on prices. Inflation is no longer a latent risk; it is becoming an active constraint on growth and macro-economic stability.

Emerging constraints

Viewed individually, many indicators point to encouraging economic performance. However, when production, business activity, trade, investment, consumption, and inflation are considered together, new constraints on growth become increasingly apparent.

Rising inflation, weak domestic demand, widening trade deficits, fragile domestic enterprises, and growing dependence on the FDI sector are creating new pressures on the economy.

These risks do not exist in isolation - they increasingly reinforce one another. Higher inflation weakens purchasing power; weaker demand limits business expansion; and when domestic firms struggle, the FDI sector gains an even larger role in driving growth. The greatest risk today is not slower growth, but growth that becomes increasingly dependent on external factors and therefore less sustainable.

Recognizing these constraints is, however, not a cause for pessimism. Rather, it is necessary to identify policy priorities more clearly as Vietnam navigates a period of overlapping challenges.

Under current conditions, the top priority for macro-economic management should be controlling inflation and safeguarding macro-economic stability. At the same time, Vietnam should continue institutional reforms, reduce compliance burdens, and lower logistics and input costs for businesses. Policies in growth support should focus more strongly on strengthening domestic enterprises, particularly manufacturers and technology companies.

With respect to FDI, the objective should not simply be attracting more capital, but attracting higher-quality investment that creates new productive capacity, transfers technology, and strengthens links with domestic enterprises. At this stage, the most important task is not merely to accelerate growth, but to protect the quality of growth.

These measures will be most effective if implemented consistently, comprehensively, and in a timely manner. More importantly, they are not just short-term responses to immediate challenges but essential steps toward reinforcing the economy’s long-term foundations.

Results in the first five months of 2026 demonstrate that Vietnam’s economy remains resilient and continues to recover. Yet new pressures are emerging more rapidly than expected.

Looking beyond this year, the greatest risk may not lie in the pace of growth itself but in the quality, autonomy, and sustainability of such growth. If domestic enterprises are not strengthened, and if growth continues to rely excessively on exports and investment from the FDI sector, the gap between economic scale and internal capacity will continue to widen.

Vietnam’s strategic objective in the years ahead should therefore extend beyond achieving faster growth. It should focus on building a more resilient economy, strengthening self-reliance, and increasing the capacity of domestic enterprises to generate higher value-added output.

In the short term, macro-economic stability and inflation control must remain the top priorities. In the long term, however, the strength of domestic enterprises will determine the economy’s resilience and global standing. High growth is important, but growth built on strong domestic foundations is the true basis for sustainable national development.

(*) Dr. Nguyen Bich Lam is the former Director General of the General Statistics Office (now the National Statistics Office under the Ministry of Finance)

Google translate

Google translate