For much of the past decade, conversations about Vietnam’s tourism industry followed a familiar script. The country was always on the cusp - rich in natural assets, strategically located, and supported by strong domestic demand - but still trailing more established markets in Southeast Asia. The consensus was clear: the opportunity was there, but it would take time.

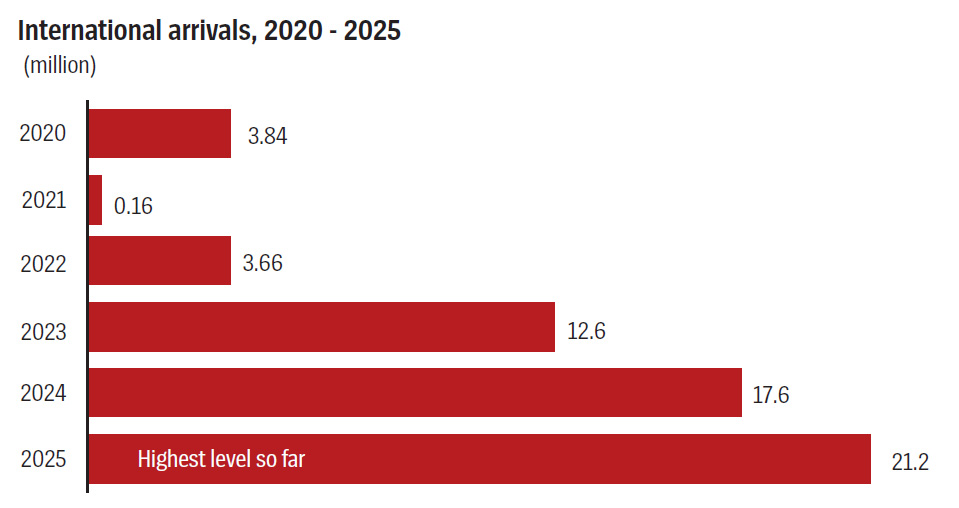

Today, that narrative has shifted. There is less speculation, more confirmation. International arrivals reached 21.5 million in 2025, surpassing pre-pandemic levels. Growth is also broadening, with secondary destinations reporting stronger occupancy, improved rates, and rising investor interest.

At Meet the Experts (MTE) HCMC 2026, discussions made clear that the story is no longer just about arrivals but about the structure behind the growth. The market is moving beyond incremental, supply-driven growth toward a more coordinated, ecosystem-based approach - one that integrates infrastructure, transport, experience, and hospitality.

From projects to ecosystems

At the center of this transformation is a new generation of Vietnamese developers, whose ambitions extend well beyond conventional real estate. For these players, hospitality is no longer an asset class in isolation. It is one component of a broader system, one that must be designed holistically if destinations are to compete at a regional and global level.

Mr. Daniel Trinh, Chief Business Development Officer at the Sun Group, articulated this shift in direct terms. “We are not just building hotels,” he said. “We actually cover the entire tourism value chain and customer journey.” Phu Quoc has become the testing ground for this philosophy. Rather than treating the island as a conventional resort destination, the Sun Group is developing it as a fully-integrated tourism ecosystem.

The starting point is access. For years, Vietnam’s tourism growth was constrained not by demand but by connectivity. Limited flight capacity, high ticket prices, and inconsistent international routes created a structural bottleneck that no amount of hotel development could overcome.

The Sun Group’s response has been to internalize that constraint. Through the launch of Sun Phu Quoc Airways, the company is not only adding capacity but actively shaping demand. Its planned expansion, from ten aircraft today to 100 by 2030, signals a long-term commitment to global connectivity. This is a critical shift. By controlling part of the transport layer, developers can influence both volume and composition of visitors, aligning demand more closely with destination positioning.

Its involvement in airport operations, combined with its collaboration with Changi Airports International, reflects recognition that the visitor experience begins long before check-in. The emphasis on “the airport as a destination” is not incidental; it mirrors global trends in which transit spaces are increasingly integrated into the broader tourism experience, shaping first impressions and influencing traveler perceptions.

Beyond external connectivity, internal mobility is also being addressed through investments such as light rail systems linking key tourism zones. As Mr. Trinh explained, for the Sun Group, this includes a light rail system connecting Phu Quoc International Airport southwards to the APEC district area, which is part of a broader effort to build the infrastructure needed for long-term destination development. These projects, while often less visible than hotels or resorts, are essential for ensuring that destinations function efficiently at scale.

The underlying logic is that tourism is not a collection of assets but a system of interdependent components. Weakness in any one element, whether transport, infrastructure, or experience, can constrain the entire ecosystem.

This thinking is increasingly shared by other Vietnamese developers. Ms. Nelly Phuong Ta, Head of Hospitality and Entertainment at the Masterise Group, said it is “not just a residential developer anymore” and is expanding into hotels, destination development, and infrastructure, including aviation and lifestyle components. Masterise’s planned airport development in northern Bac Ninh province illustrates how infrastructure is becoming a strategic tool for shaping regional tourism flows. By creating new gateways, developers can redistribute demand, reduce pressure on existing hubs, and unlock new destinations.

Meanwhile, Ms. Thu Le, CEO of T&T Hospitality, emphasized the importance of master planning at scale. With land banks extending up to 1,000 ha, the company is focusing on creating integrated destinations that combine accommodation with cultural, recreational, and experiential components.

The Group, she said, is focusing on attraction activities to build a place as a destination, and careful master planning is essential “in order not to turn it to an empty ghost town.” This observation touches on a critical challenge in Vietnam’s development cycle. Rapid expansion of supply, if not matched by demand generation and experience design, can lead to underutilization, a pattern observed in several emerging markets globally.

Amid the growing focus on large-scale, integrated developments, some investors are taking a more fundamentals-driven approach. Mr. Nguyen Duc Minh, CEO of One Capital Hospitality, emphasized that while the market is evolving, the core drivers of successful hospitality investment remain unchanged.

Drawing on a principle often cited in business strategy, Mr. Minh emphasized that successful hotel investment still comes down to three core elements: location, service, and story. “It is difficult to imagine a guest rejecting a hotel because it is well-located, offers excellent service, and has a compelling narrative,” he said, noting that they provide a stable foundation in a market otherwise defined by rapid transformation. This perspective has guided the company’s focus on destinations such as Hanoi and Nha Trang, where these fundamentals are already well established.

Rewriting the rules

While developers are redefining destinations at the macro level, operators are reshaping the micro-level dynamics of hospitality. This transformation is driven by changing traveler behavior, shifting cost structures, and the increasing importance of distribution.

Mr. Michael Piro, Co-CEO and Board Member at Indochina Capital, framed this evolution through the lens of Wink Hotels. The brand was conceived as a response to a structural gap in the market, one between high-end luxury and underwhelming midscale offerings. But beyond product positioning, Wink represents a rethinking of operational fundamentals.

By eliminating non-essential amenities and focusing on core revenue drivers, the brand achieves a level of efficiency that is critical in a price-sensitive, high-growth market. The model - one staff member per five rooms, 24-hour operations, and a strong emphasis on room yield - reflects a disciplined approach to profitability.

Yet the most significant insight from Wink’s development lies elsewhere. Mr. Piro noted that while real estate focuses on location, hospitality is ultimately driven by distribution. This shift from physical to digital and network-based advantage is reshaping competitive dynamics across the industry. Visibility, access to loyalty programs, and integration into global booking systems are increasingly decisive factors.

Wink’s partnership with Hyatt illustrates how local brands can leverage global platforms without losing identity. By joining the “Unscripted by Hyatt” collection, the brand gains access to a large loyalty base and distribution network while maintaining operational independence. The early results - higher occupancy, increased average daily rates, and longer guest stays - underscore the importance of this strategy.

For the Fusion Hotel Group, distribution is being addressed through platform integration. The Group was acquired in March 2026 by Mr. Suchad Chiaranussati, Founder and Chairman of SC Capital Partners, as part of a strategy to expand its footprint in Asia’s hospitality sector. The deal positions Fusion within a broader platform that also includes Hotel Management Japan (HMJ) and the Indonesia-based Topotels Hotels & Resorts, with the combined portfolio managing approximately 16,000 rooms across key markets in the region.

Mr. David Roberts, Group Chief Operating Officer at the Fusion Hotel Group, explained how the company’s alignment with SC Capital Partners enables a hybrid model combining ownership and operations across multiple markets. This structure allows for greater control over asset pipelines, faster expansion, and shared commercial capabilities. He said the goal was “to create a pan-Asian hospitality company,” adding that the platform is already being integrated across markets through joint expansion, shared commercial strategies, and loyalty programs.

At the same time, alternative models are entering the market. Club Med’s approach, as described by Mr. Sebastien Favre, Vice President of Development, Construction & Asset Management, SEA & Pacific, at Club Med, represents a fundamentally different logic. By combining product and distribution within a single platform, the company can effectively generate demand for destinations that would otherwise struggle to attract visitors. This capability is particularly relevant for Vietnam, where many potential destinations remain underdeveloped. The ability to “activate” these locations through integrated models could accelerate the country’s geographic diversification.

Meanwhile, established operators such as Dusit International are taking a more measured approach, prioritizing differentiation over rapid expansion. Mr. Siradej Donavanik, Vice President - Development (Global) at Dusit International, emphasized that while the group has the flexibility to deploy a wide portfolio of brands, from ultra-luxury to midscale lifestyle concepts, growth in Vietnam will remain deliberately selective.

Rather than pursuing scale for its own sake, Dusit aims to add only a limited number of properties each year, ensuring that each project meaningfully reinforces the brand. This approach is already reflected in its recent expansion, including a newly-opened property in Hanoi, which Mr. Donavanik highlighted as part of the group’s growing footprint in the country.

For Dusit, the focus is firmly on experience, wellness, and the essence of Asian hospitality. He said the group is “not really into the numbers game,” instead focusing on ensuring that each property “activates the brand” and is co-created from the outset. This philosophy extends to how the company partners and operates. As both an owner and manager, Dusit emphasizes long-term relationships and early-stage collaboration with developers, ensuring that each project is carefully positioned from the outset. In this model, success is not defined by the speed of expansion but by how well each property delivers a distinctive experience and contributes to the broader destination.

Infrastructure & strategy

Across the discussion, despite the diversity of business models and development strategies, one point of alignment was clear: infrastructure will ultimately determine how far Vietnam’s tourism sector can go. Growth is no longer constrained by demand alone, but by how effectively the country can support and channel that demand.

As Mr. Piro put it, the issue is fundamentally one of access. “If you cannot get people to these destinations, no matter how many hotel rooms we build, it’s not going to make a difference.” His point reflects a broader concern shared across the panel, that without sufficient connectivity, even the most ambitious developments risk underperforming.

Vietnam’s infrastructure pipeline is expanding, with major projects expected to increase airport capacity and improve accessibility. However, the discussion highlighted that infrastructure is not simply about adding capacity. It is also about how well different components work together. Airports, roads, and internal transport systems must operate as a coordinated network. Gaps or inefficiencies at any stage of the journey can weaken the overall destination experience.

There is also a question of timing. Infrastructure needs to keep pace with development. If hotel supply grows faster than connectivity, bottlenecks will emerge, limiting both occupancy and visitor satisfaction. At the same time, the panel suggested that infrastructure should not be viewed in isolation, but as part of a broader system that includes attractions, entertainment, and supporting services.

Everyone was looking at international arrivals, but domestic travel is enormous and it continues to grow. We saw it outstripping international quite significantly. That was the key opportunity for us.

Beyond physical connectivity, the discussion also highlighted the importance of branding, marketing, and destination positioning. This includes how Vietnam positions itself in the global market and how effectively it communicates the quality of its destinations.

Mr. Roberts noted that interest in Vietnam is already strong across regional and international markets. The next step, however, is to convert that interest into sustained demand. This requires clearer messaging around what Vietnam offers, not just in terms of availability, but in terms of experience and differentiation.

This leads directly to a deeper strategic question that emerged in discussions: whether Vietnam should prioritize quantity or quality in its next phase of growth. As the market matures, the focus is beginning to shift from simply increasing visitor numbers to enhancing value. For Mr. Piro, this is a critical inflection point. “Vietnam will have a choice,” he said. “Do we want to focus on quality or quantity? At what point do we become a yielding market where we really focus on rate growth rather than just expanding numbers.” Long-term success, he emphasized, will depend on how much value each visitor brings, rather than how many arrive.

What’s really important for us is to stay focused on the experience. At the core, we want to focus on the experience economy, particularly wellness and Asian hospitality, which remain central to what we do.

This perspective carries broader implications across the industry. For developers, it suggests a move toward more integrated, experience-driven destinations rather than standalone projects. For operators, it points to the importance of brand positioning and guest experience. For the market as a whole, it raises questions about sustainability and long-term competitiveness.

In that context, the industry is no longer defining success purely in terms of expansion. Instead, it is beginning to focus on how that expansion is structured and what it ultimately delivers. Vietnam’s tourism sector has clearly moved beyond its early stage of growth. Demand is strong, investment is accelerating, and new models are being introduced across the market. The more important question now is how these elements come together. If infrastructure, positioning, and development strategies can be aligned, Vietnam has the potential to sustain its momentum and strengthen its position in the region.

There’s a ton of interest coming from Asia-Pacific and other regions, now it’s how do we get the message out about the quality of the destinations that we have in Vietnam.

![[Interactive]: Economic overview - June 2026](https://premedia.vneconomy.vn/files/uploads/2026/07/04/93e55a21c3a54d4fa07397ef62fcca05-102490.png?w=400&h=225&mode=crop)

Google translate

Google translate